1Department of Information Management, Faculty of Business Management,

Bratislava University of Economics and Business, Bratislava, Slovak Republic (EU)

2Department of Business Economy, Faculty of Business Management,

Bratislava University of Economics and Business, Bratislava, Slovak Republic (EU)

Volume 2026,

Article ID 833707,

IBIMA Business Review,

20 pages,

DOI: doi.org/10.5171/2026.833707

Received date: 30 March 2026; Accepted date: 5 May 2026; Published date: 1 June 2026

Academic Editor: Karlis Kreslins

Cite this Article as:

Anita ROMANOVA, Matej CERNY and Peter STETKA (2026), "The Mediating Role of Economic IT Evaluation between IT Governance and Organizational Outcomes: Evidence from Slovak Enterprises“, IBIMA Business Review, Vol. 2026 (2026), Article ID 833707, https://doi.org/10.5171/2026.833707

In the context of the IT productivity paradox, this study examines how formal IT governance (ITG) and the institutionalized use of economic metrics for IT evaluation relate to the organizational outcomes of technological innovations in enterprises operating in Slovakia. While prior research confirms the importance of ITG and systematic IT evaluation separately, limited evidence explains whether the ITG–outcome relationship is direct or operates indirectly through economic evaluation routines, particularly in Central and Eastern European settings. Drawing on a cross-sectional questionnaire survey of 286 enterprises, the study applies descriptive statistics, Mann–Whitney U tests, chi-square tests of independence, binary logistic regression, and a bootstrap mediation analysis with 5,000 resamples. The results show that organizations with formal ITG exhibit a significantly stronger strategic positioning of ICT (OR = 3.445, p < .001), while the use of economic metrics is associated with higher perceived benefits of technological innovations for competitiveness, responsiveness to market changes, and competitive advantage. In the multivariate model, formal ITG did not directly predict reported operating cost reduction, whereas the use of economic metrics remained a significant predictor (OR = 4.576, p < .001). The mediation analysis confirmed an indirect-only mediation pattern, with a significant indirect effect (ab = 2.09, 95% CI [0.82, 4.76]) and a non-significant direct effect. The findings support the resource complementarity perspective and suggest that governance structures create value primarily when combined with systematic economic evaluation routines.

Keywords: IT governance; economic evaluation of IT; organizational outcomes; mediation.

Introduction

The digitization of business processes has become a strategic imperative for organizations seeking to increase operational efficiency and maintain competitiveness in a fast-paced, technology-driven environment (Adomako & Nguyen, 2023; Rubio-Andrés et al., 2025). In today’s environment, technologies are no longer an end in themselves but a means of creating value. However, their contribution to organizational effectiveness depends on the digital transformation strategy and how IT resources are governed and managed (Rubio-Andrés et al., 2025).

A key mechanism for achieving these goals is IT governance (ITG), defined as a set of leadership, organizational structures, and processes ensuring that IT within the organization supports and advances strategies and objectives (Tahar et al., 2021; Karataş & Çakır, 2024). Effective ITG provides the stable, secure platform and business-IT alignment necessary to extract real value from technology investments (Harguem, 2021; Panda, 2022). The presence of formal structures is considered an indicator of ITG maturity and a prerequisite for its strategic effectiveness (Harguem, 2021; Pashutan et al., 2022).

Despite investments in digitalization, organizations still struggle to demonstrate the concrete and measurable value of IT (Töhönen et al., 2020). The IT productivity paradox suggests that IT investments alone do not automatically lead to increased organizational performance (Schweikl & Obermaier, 2022). An explanation is offered by the theory of resource complementarity. IT creates value only in combination with complementary organizational resources, such as governance mechanisms and systematic economic evaluation (Schweikl & Obermaier, 2022; Töhönen et al., 2020). Evaluating IT benefits is challenging due to its intangible nature, the time lag between implementation and results, and the distinction between technical efficiency and strategic business performance (Töhönen et al., 2020; Yang et al., 2025).

Technological innovations and process digitization can lead to increased operational efficiency, agility in responding to market changes, and a strengthened competitive position (Adomako & Nguyen, 2023). These benefits do not materialize automatically. They depend on how technological initiatives are managed, aligned with business objectives, and systematically evaluated (Pashutan et al., 2022). This article is based on the assumption that formal ITG and the institutionalized use of economic metrics for IT evaluation represent key organizational prerequisites for transforming ICT into a strategic role, achieving higher perceived benefits from innovation, and effectively reducing operating costs (Harguem, 2021). From the perspective of dynamic capabilities (Harguem, 2021), it can be assumed that the relationship between ITG and organizational outcomes may not be direct. It may be mediated by a system of economic evaluation that enables the transformation of IT investments into concrete, measurable benefits.

This article empirically tests whether the relationship between formal ITG and reported organizational outcomes is mediated by the systematic use of economic IT evaluation metrics. Attention is paid to verifying the robustness of the identified mediation pattern after accounting for organization size and sector, which the literature defines as significant contextual factors of digital transformation. The article contributes to the IT business value literature by integrating formal governance structures, economic evaluation routines, and perceived organizational outcomes within a single mediation-based empirical model.

Theoretical Background

The present study builds on three complementary theoretical perspectives that jointly explain how IT governance translates into organizational outcomes: the resource-based view (RBV), the dynamic capabilities perspective, and resource complementarity.

The resource-based view (Barney, 1991) argues that sustained competitive advantage arises from organizational resources that are valuable, rare, inimitable, and non-substitutable. Applied to information systems, Wade and Hulland (2004) emphasize that IT assets become strategically relevant only when bundled with complementary organizational capabilities; neither IT resources nor management practices are sufficient in isolation. Bharadwaj (2000) extends this logic by defining IT capability as the combined set of IT infrastructure, human IT resources, and IT-enabled intangibles, showing that this bundle, rather than IT spending alone, predicts superior firm performance.

The dynamic capabilities perspective (Teece, Pisano and Shuen, 1997; Eisenhardt and Martin, 2000) focuses on the firm’s ability to integrate, build, and reconfigure internal and external competences to address rapidly changing environments. In the IT context, formal ITG structures can be understood as organizational routines that enable sensing, seizing, and reconfiguring of IT resources in response to changing business requirements. Harguem (2021) explicitly links ITG mechanisms to dynamic capabilities, arguing that structural and process-based ITG develops IT management capabilities, which in turn enable strategic business–IT alignment and organizational performance.

Resource complementarity theory (Melville, Kraemer and Gurbaxani, 2004; Schweikl and Obermaier, 2022) synthesizes these insights by explaining the IT productivity paradox. IT creates value only when combined with complementary organizational, human, and managerial resources. Kohli and Grover (2008) further argue that the value of IT evolves from efficiency gains to strategic enablement and requires organizational mechanisms, notably governance and evaluation routines, to be realized in practice.

Together, these perspectives motivate the central theoretical argument of this study: formal ITG establishes the structural precondition for strategic IT value, but actual translation of governance into measurable organizational outcomes depends on systematic economic evaluation of IT investments as a complementary routine. This yields a mediated relationship in which economic evaluation carries the governance–outcome linkage, rather than an immediate direct effect of structural governance on reported cost savings.

Empirical tests of such mediation typically follow the Preacher and Hayes (2008) bootstrap approach, which provides robust estimates of indirect effects without the distributional assumptions required by older Baron and Kenny (1986) causal-steps logic. The typology of Zhao, Lynch and Chen (2010) further distinguishes between indirect-only (formerly full), complementary (formerly partial), and competitive mediation patterns, providing a more nuanced interpretive framework than the traditional full-versus-partial dichotomy. This theoretical apparatus guides both the hypotheses developed below and the mediation analysis reported in the Results section.

Literature Review

IT is considered a prerequisite for organizational success, as it influences how firms create and capture value and how they respond to competitive pressures (Elazhary et al., 2023; Kumar et al., 2024).

ITG is an integral part of corporate governance and management, encompassing leadership, organizational structures, and processes that ensure IT supports and advance the organization’s strategies and objectives (Karataş & Çakır, 2024; Harguem, 2021; Tahar et al., 2021). Unlike IT management, which focuses primarily on the operational management of IT services and current IT operations, ITG has a broader strategic orientation. It focuses on the direction of IT, its transformative role, and alignment with business needs (Karataş & Çakır, 2024). In practice, ITG relies on recognized frameworks that provide a structured approach to IT management. Patterson (2020) identifies COBIT 5 as the dominant governance framework, which maps 37 processes to business imperatives and integrates Val IT principles for evaluating IT investments. ITIL is also frequently cited as a framework for IT service management, complementing COBIT’s strategic orientation with an operational dimension (Karataş & Çakır, 2024; Patterson, 2020).

Effective ITG is most understood through three types of mechanisms: structural, process-based, and relational (Karataş & Çakır, 2024; Harguem, 2021). Structural mechanisms involve the creation of organizational units, formal roles, and responsibilities, while process mechanisms relate to the formalization of strategic IT planning, monitoring, and control (Harguem, 2021; Karataş & Çakır, 2024; Elazhary et al., 2023). The presence of a separate IT department or a formal managerial role can thus be considered a manifestation of higher ITG formalization and one of the indicators of organizational maturity (Harguem, 2021; Elazhary et al., 2023).

From a theoretical perspective, the relationship between ITG mechanisms and organizational outcomes is increasingly explained through dynamic capabilities. Harguem (2021) proposes a framework in which structural, process, and relational ITG mechanisms develop IT management capabilities, which in turn enable strategic alignment of IT with the business and lead to organizational performance. Panda (2022) found that strategic alignment between IT and business supports organizational performance, with organizational agility acting as a significant mediator. Elazhary et al. (2023) add to this finding by noting that ITG influences organizational agility through IT capabilities, with market turbulence remaining a significant moderator.

The central goal of ITG is to achieve strategic alignment between business and IT—that is, a state in which IT priorities, objectives, and decisions are coordinated with corporate strategy and support the creation of value from IT investments (Harguem, 2021; Patterson, 2020). A higher level of formalization of governance mechanisms is associated with IT becoming a strategic partner of the organization that actively contributes to the achievement of corporate goals. Therefore, we hypothesize that the existence of formal ITG will be positively associated with the strategic role of IT in the organization (H1).

It is increasingly important for management to demonstrate IT business value, i.e., the contribution to organizational performance at both the operational and strategic levels (Schweikl & Obermaier, 2022; Maia & Frogeri, 2023). Measuring these benefits is challenging, as the impacts are often intangible, indirect, and manifest with a time lag between investment and outcome (Töhönen et al., 2020; Yang et al., 2025).

The Solow paradox describes a situation where IT investments do not automatically lead to increased organizational performance. Based on an integrative review of 227 studies, Schweikl and Obermaier (2022) show that the key to explaining this paradox is the concept of resource complementarity. IT creates value only in combination with complementary organizational resources, such as managerial capabilities, organizational culture, and governance mechanisms. Töhönen et al. (2020) add that the value of IT is systemic and emerges from interactions between IT and the organizational context, while traditional financial metrics often fail to capture this complexity. These findings suggest that the mere existence of ITG may be insufficient without a systematic economic evaluation of IT.

Economic metrics for IT evaluation are not merely financial indicators but also tools that can support more economically rational decision-making regarding IT investments (Töhönen et al., 2020; Karataş & Çakır, 2024). Their systematic use can help better assess the expected benefits of technology projects and reduce uncertainty (Töhönen et al., 2020; Pashutan et al., 2022).

Although financial evaluation cannot fully capture all intangible effects of IT, its use can contribute to greater consistency and transparency in IT resource management (Schweikl & Obermaier, 2022). We hypothesize that the use of economic metrics for IT evaluation is associated with higher perceived benefits of technological innovations (H2).

Technological innovations and process digitization are significant factors in business modernization, as they contribute to process transformation, increased efficiency, and improved organizational performance (Kumar et al., 2024; Rubio-Andrés et al., 2025). The benefits of these innovations are primarily associated with strengthening competitiveness, better responding to changing market conditions, and strengthening competitive advantage (Rubio-Andrés et al., 2025; Elazhary et al., 2023). Digitalization fosters organizational agility, that is, the ability to respond flexibly to changes in the environment and adapt resources and processes (Elazhary et al., 2023). Technological innovations can also have cost implications, as automation and process optimization are often associated with increased operational efficiency and reduced costs (Rubio-Andrés et al., 2025).

Therefore, we hypothesize that the use of economic IT evaluation metrics mediates the relationship between formal ITG and reported reductions in operating costs resulting from technological innovations. While formal ITG creates the structural framework for managing innovations, systematic economic evaluation represents the complementary routine through which governance is translated into measurable cost outcomes. (H3).

The literature on business-IT misalignment examines the consequences of insufficient alignment. Őri and Szabó (2024) identify that misalignment leads to reduced organizational performance, suboptimal use of IT, and the organization’s inability to respond to changes in the external environment. The authors emphasize the dominant role of the Henderson-Venkatraman Strategic Alignment Model (SAM) as the theoretical foundation for this field and note that the absence of formal governance mechanisms is one of the main causes of misalignment.

The relationship between ITG and organizational outcomes must be assessed regarding the organization’s context. The appropriateness of governance mechanisms may vary depending on the size of the organization and other organizational characteristics, with firm size and sector often considered as control variables (Harguem, 2021; Merín-Rodrigáñez et al., 2024) (H4).

Research Framework and Methodology

This article verifies whether formal ITG and the use of economic IT evaluation metrics are associated with more favorable organizational outcomes in companies in Slovakia. The research focuses on the relationship between the existence of formal ITG and the strategic role of IT in the organization, on the association between the use of economic IT evaluation metrics and the perceived benefits of technological innovations, as well as on assessing whether these relationships persist even after controlling for organization size and sector. The following null and alternative hypotheses were formulated:

H1₀: There is no positive association between the existence of a formal ITG, operationalized as the presence of a separate IS/IT department or an IT manager, and the strategic role of ICT in the organization.

H1: There is a positive association between the existence of a formal ITG, operationalized as the presence of a separate IS/IT department or an IT manager, and the strategic role of ICT in the organization.

H2₀: Organizations that use economic metrics for IT evaluation do not report higher perceived benefits of technological innovations in terms of competitiveness, responsiveness to market changes, and competitive advantage.

H2: Organizations that use economic metrics for IT evaluation report higher perceived benefits of technological innovations in terms of competitiveness, responsiveness to market changes, and competitive advantage.

H3₀: The use of economic IT evaluation metrics (e.g., ROI, TCO, OPEX, CAPEX) does not mediate the relationship between formal ITG and reported reductions in operating costs resulting from technological innovations.

H3: The use of economic IT evaluation metrics (e.g., ROI, TCO, OPEX, CAPEX) mediates the relationship between formal ITG and reported reductions in operating costs resulting from technological innovations.

H4₀: After controlling for organization size and sector, the associations between formal ITG, the use of economic IT evaluation metrics, the strategic role of ICT, and reported operating cost reduction do not persist.

H4: After controlling for organization size and sector, the associations between formal ITG, the use of economic IT evaluation metrics, the strategic role of ICT, and reported operating cost reduction persist.

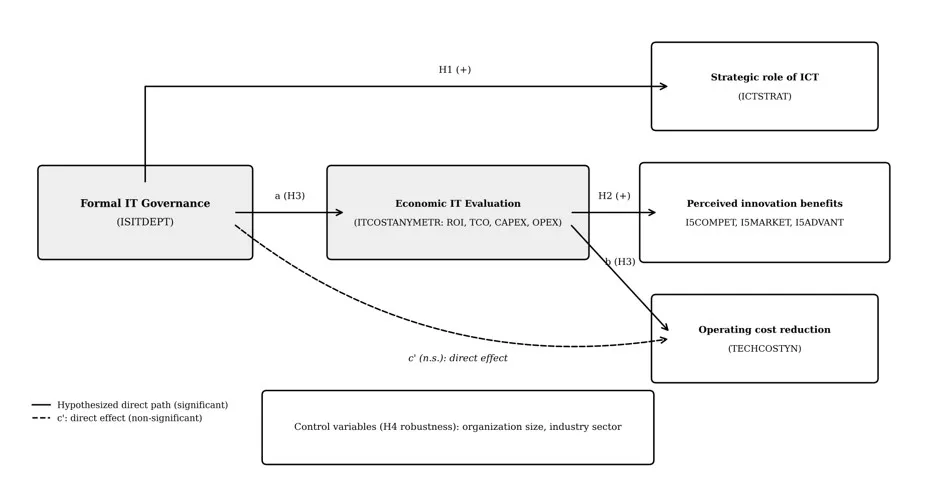

Fig. 1 summarises the research framework. It positions formal IT governance as the independent variable, the institutionalized use of economic IT evaluation metrics as the mediator, and three organizational outcomes as dependent variables: the strategic role of ICT, perceived innovation benefits, and reported operating cost reduction. Hypotheses H1 and H2 test the direct relationships from formal ITG to the strategic role of ICT and from economic evaluation to perceived innovation benefits, respectively. Hypothesis H3 operationalises the mediation chain: path a captures the effect of formal ITG on the use of economic evaluation, path b captures the effect of economic evaluation on operating cost reduction, and c’ denotes the residual direct effect of formal ITG on cost reduction. Hypothesis H4 asks whether the associations between formal ITG, the use of economic IT evaluation metrics, the strategic role of ICT, and reported operating cost reduction persist after controlling for organization size and sector.

Fig. 1. Research framework — mediation model of IT governance, economic IT evaluation, and organizational outcomes. Indirect effect ab = 2.09, 95% bootstrap CI [0.82, 4.76]. Source: prepared by the authors.

This study employed a quantitative, cross-sectional research design based on a questionnaire survey administered to business organizations operating in Slovakia. Given the exploratory character of the research and the still limited empirical evidence on firm-level ITG and Industry 5.0 implementation in Central European economies, non-probability convenience sampling was used. The firm served as the primary unit of analysis, and data were collected from organizational respondents representing enterprises of different sizes, ownership structures, and sectors of economic activity.

The questionnaire was administered online between January and June 2025. It comprised multiple thematic blocks covering digital maturity, information strategy, ITG, IT economic evaluation, readiness and need for Industry 5.0, implementation barriers, and perceived organizational outcomes. The item pool was developed from the literature review and adapted to the Industry 5.0 and ITG context. Perceptual items were measured on seven-point ordinal scales ranging from 0 (not important / insignificant / none) to 6 (very important / strategic). Binary indicators (e.g., the existence of a formal IS/IT unit, or the use of economic IT evaluation metrics) were captured using single questionnaire items.

After data screening, 286 complete and usable responses were retained for the analyses reported in this study. Although the resulting sample is analytically informative and heterogeneous across firm size, ownership structure, and sector of economic activity, the use of convenience sampling means that the results should be interpreted as analytically informative rather than statistically representative of the entire population of firms operating in Slovakia.

The ORGSIZE variable was derived from the number of employees (EMPS2024) according to enterprise size criteria based on European Commission Recommendation 2003/361/EC (European Commission, 2003). Organizations were classified as micro-enterprises (up to 9 employees) – 21%, small enterprises (10–49 employees) – 29.7%, medium-sized enterprises (50–249 employees) – 23.8%, and large enterprises (250 or more employees) – 25.5%.

The original sector variable was transformed into broader analytical blocks (SECTORIND_TRANSFORMED, reduced from 19 NACE-based categories into 6 analytical blocks) because the detailed categories had low frequencies and could lead to unstable estimates. Classifications derived from NACE are aggregated into broader sectoral groups according to the analytical objective of the study.

Table 1. Frequency table by transformed sector variable

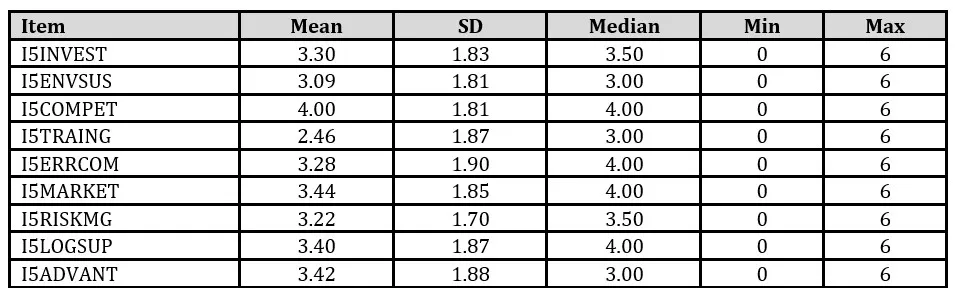

Variables capturing the formal and substantive aspects of ITG were used in hypothesis testing. The existence of a separate IT department or IT manager (ISITDEPT; 0 = no, 1 = yes) was used as the key independent variable. The strategic position of ICT in the company was operationalized by the variable ICTSTRAT, measured on an ordinal scale from 0 to 6, where higher values indicate a more strategic role for ICT. The area of economic evaluation of IT was captured through indicators of the use of TCO, ROI, CAPEX, and OPEX metrics, whereby for analytical purposes it was possible to work either with a binary indicator of the use of at least one metric (ITCOSTANYMETR) or with the number of metrics used (ITCOSTCOUNT). Performance and perceptual effects of digitalization and readiness for Industry 5.0 were tracked using nine items measured on an ordinal scale from 0 to 6. These items captured the required level of investment for the transition to Industry 5.0 (I5INVEST), environmental sustainability (I5ENVSUS), the organization’s future competitiveness (I5COMPET), employee readiness in terms of education and skills (I5TRAING), reduction of errors and complaints (I5ERRCOM), ability to respond to market changes (I5MARKET), ability to anticipate and manage risks (I5RISKMG), improvement of logistics and supply chains (I5LOGSUP), gaining a competitive advantage through modern technologies (I5ADVANT), and also the variable TECHCOST, expressing the percentage reduction in operating costs resulting from technological innovations.

The Mann-Whitney U test was used to test H1 and H2, since in both cases the independent variables divided the sample into two independent groups and the dependent variables were measured on an ordinal scale from 0 to 6. For H1, the relationship between the existence of an IT department (ISITDEPT) and the degree of strategic ICT alignment (ICTSTRAT) was analyzed. H2 examines the relationship between the use of economic metrics for IT evaluation (ITCOSTANYMETR) and indicators of the perceived benefits of technological innovations (I5COMPET, I5MARKET, I5ADVANT). Testing was performed separately for each dependent variable. p-values were adjusted using the Holm-Bonferroni procedure. In both cases, the parametric assumption was also examined; for H1, Levene’s test indicated a violation of homogeneity of variances, while, for H2, this assumption was not violated. Given the ordinal nature of the variables, a nonparametric test was chosen as the primary analytical procedure in both cases. Effect size was also included in the interpretation to assess the practical significance of the observed differences (Altman & Bland, 2009; MacFarland & Yates, 2016).

The choice of tests for H3 was based on the type of variables analyzed. Since TECHCOSTYN is a binary variable and ISITDEPT and ITCOSTANYMETR are dichotomous variables, chi-square tests of independence were used to verify bivariate relationships (Poldrack, 2018). To assess the combined effect of both factors, a 4-category typology was created and analyzed using the same test, with the interpretation of individual cells supplemented by standardized residuals. Binary logistic regression was used for multivariate hypothesis testing, which allowed modeling the probability of TECHCOSTYN = Yes while simultaneously accounting for other variables (Harris, 2021).

H4 was tested using binary logistic regression. The dependent variable was TECHCOSTYN (0 = no, 1 = yes). ISITDEPT and ITCOSTANYMETR were included as main predictors, and ICTSTRAT was included in the extended model; control variables consisted of ORGSIZE and economic activity sector. ICTSTRAT was treated as a contextual organizational characteristic in the extended specification rather than as a purely exogenous control variable; its inclusion therefore serves as a robustness check of whether the observed associations persist when the strategic positioning of ICT within the organization is taken into account. This approach is suitable for a dichotomous dependent variable and a combination of binary, categorical, and ordinal predictors (Harris, 2021).

As a supplementary analysis, a binary logistic regression was also estimated for H1 with the dichotomized dependent variable ICTSTRAT (≥ 4 vs. < 4) and the predictors ISITDEPT, ORGSIZE (log-transformed), sector, and ownership, to verify the robustness of the bivariate finding in a multivariate setting. The quality of all logistic regression models was assessed using several diagnostic indicators: the omnibus test (likelihood ratio χ²) to verify the overall significance of the model, Nagelkerke's R² and Cox & Snell R² to assess explained variance, the Hosmer-Lemeshow test to evaluate model fit, and a classification table (accuracy, sensitivity, specificity) to assess the model's predictive ability. Effect size for chi-square tests was evaluated using the Phi coefficient (for 2 × 2 tables) and Cramer's V (for larger tables).

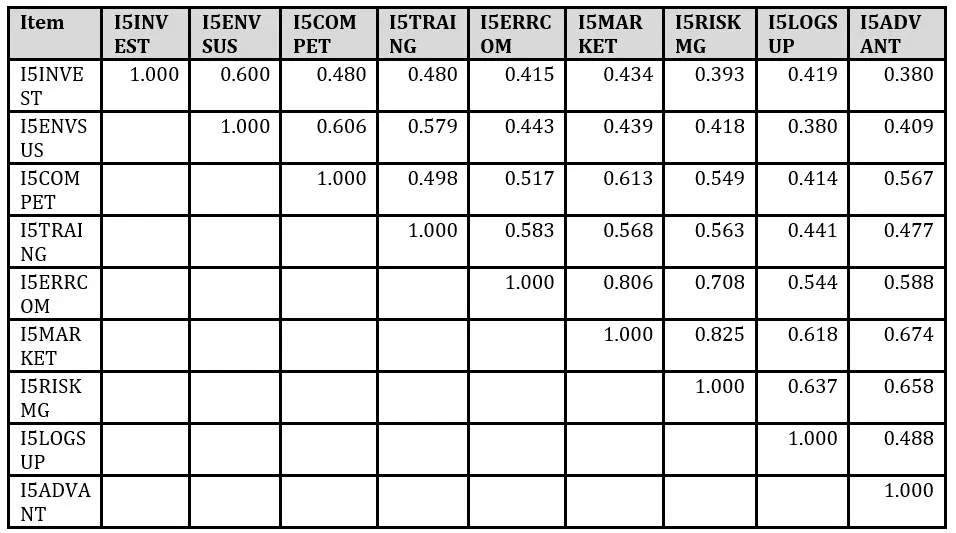

Although the nine items (I5INVEST, I5ENVSUS, I5COMPET, I5TRAING, I5ERRCOM, I5MARKET, I5RISKMG, I5LOGSUP, I5ADVANT) capture distinct dimensions of perceived organizational impact, they share a common underlying construct, namely the overall perceived organizational impact of Industry 5.0 transformation. Treating these items as a composite scale is consistent with prior empirical practice in IT business-value and organizational-readiness research, where aggregated perceptual indicators are used to assess internal consistency of higher-order constructs (Hair et al., 2019; Nunnally & Bernstein, 1994). Cronbach’s alpha for the nine-item composite was α = 0.915, indicating excellent internal consistency. A sub-scale constructed from the three H2 outcome items (I5COMPET, I5MARKET, and I5ADVANT), representing perceived competitive benefits of technological innovation, yielded α = 0.827, also indicating high internal consistency. Convergent validity was further supported by the average Spearman inter-item correlation of r̅ = 0.534 (all p < 0.001), with the strongest pairwise correlations between I5MARKET and I5RISKMG (ρ = 0.825), I5MARKET and I5ERRCOM (ρ = 0.806), and I5MARKET and I5ADVANT (ρ = 0.674). The remaining variables (ISITDEPT, ITCOSTANYMETR, ICTSTRAT, TECHCOSTYN) were measured as single-item indicators, for which reliability assessment through Cronbach's alpha is not applicable.

To assess common method bias (CMB), Harman’s test was performed using a one-factor model. Unrotated PCA was applied to the 9 Likert scale items from the question: Performance and perceptual effects of digitalization and readiness for Industry 5.0. The results showed that the first component explained 59.89% of the total variance, exceeding the conventional threshold of 50%. This indicates a moderate CMB effect, which may overestimate correlations by approximately 10–15%. At the same time, however, a multi-factor structure was identified (second component = 11.35%, third = 6.58%), suggesting that not all variance is method related

Multicollinearity among the predictors was tested using variance inflation factors (VIF). All VIF values were well below the conventional threshold of 5.0: ITG (VIF = 1.564), economic metrics (VIF = 1.214), organization size (VIF = 1.582), sector (VIF = 1.041), and ownership (VIF = 1.150).

To formally assess whether the relationship between formal ITG and organizational outcomes is mediated by the systematic use of economic IT evaluation metrics, a bootstrap mediation analysis was performed following the Preacher and Hayes (2008) PROCESS Model 4 framework. Compared with the causal-steps approach of Baron and Kenny (1986), bootstrap resampling provides more robust indirect-effect estimates without distributional assumptions (Hayes, 2017). The resulting pattern is interpreted using the typology of Zhao, Lynch and Chen (2010), which distinguishes between indirect-only, complementary, and competitive mediation rather than the traditional full-versus-partial dichotomy. Because all three analytic variables (X, M, Y) are binary, the mediator and outcome models are estimated as logistic regressions; the indirect effect is computed as the product of path coefficients on the log-odds scale. Confidence intervals for direct, indirect, and total effects are obtained from 5,000 bootstrap resamples (95% percentile method). Covariates in both path equations include ICTSTRAT, organization size, and the aggregated sector variable, mirroring the controls used in the multivariate regressions reported for H3 and H4.

Results and Discussion

H1 hypothesized a positive association between the existence of a formal ITG and the strategic role of ICT in the organization. For empirical verification, the Mann-Whitney U test was used to compare the distribution of values for the ICTSTRAT variable between organizations with and without a formal ITG.

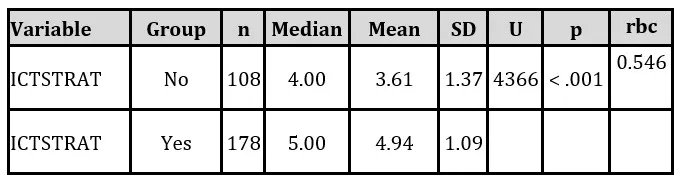

Table 2. Comparison of the strategic position of IT based on the existence of a separate IT department or IT manager

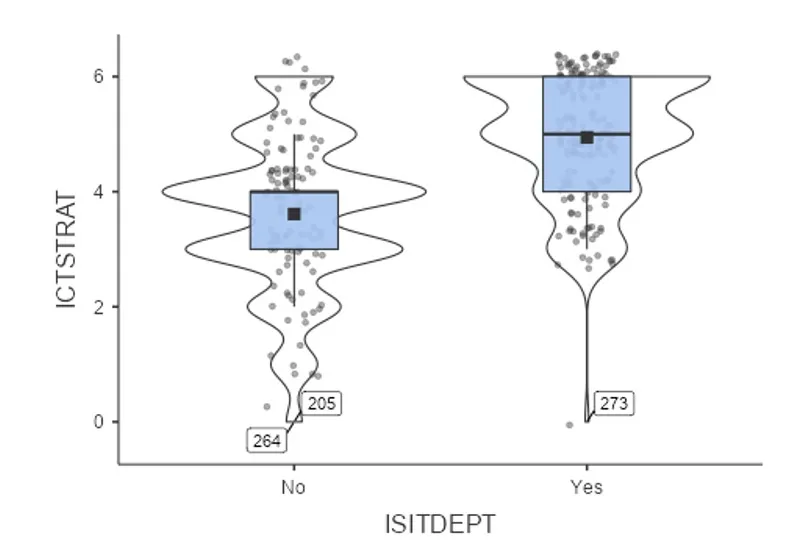

The analysis confirmed a statistically significant difference in the ICTSTRAT variable, U = 4366, p < .001, with organizations having a formal ITG exhibiting a higher level of the strategic role of ICT (Mdn = 5.00; M = 4.94; SD = 1.09; n = 178) than organizations without a formal ITG (Mdn = 4.00; M = 3.61; SD = 1.37; n = 108). The observed effect was also substantively significant in terms of effect size (rank-biserial correlation /rbc/ = .546). The distribution of ICTSTRAT was skewed towards higher strategic perception, with 27.3% of respondents choosing the maximum value (6 = Strategic) and only 1.0% choosing 0 (None). Based on these results, H1wassupported.

A supplementary binary logistic regression confirmed the robustness of this finding. The model with ITG as the main predictor (controlled for size, sector, and ownership) was statistically significant, χ²(4) = 42.85, p < .001, Nagelkerke’s R² = 0.139. The Hosmer-Lemeshow test confirmed good model fit with the data (χ² = 7.67, p = .467). Organizations with a formal ITG were 3.4 times more likely to have a strategic perception of ICT (OR = 3.445, 95% CI [1.754–6.769], p < .001). Organization size (log-transformed employees) also emerged as a significant predictor (OR = 1.282, p = .012), indicating that larger organizations tend to exhibit a more strategic perception of ICT. The model’s overall classification accuracy reached 76.2% with a sensitivity of 93.9%.

These results are consistent with empirical findings in the literature. Elazhary et al. (2023) found that ITG positively influences IT capability (β = 0.697, p < 0.01), which in turn enhances organizational agility. Tahar et al. (2021) reported a significant direct effect of ITG on organizational performance (β = 0.259, p = 0.009), which is comparable to our finding OR = 3.445. Panda (2022) also confirmed that strategic alignment between IT and business predicts organizational performance, with organizational agility acting as a significant mediator. Our findings thus support the broader consensus that formal ITG is an important predictor of the strategic importance of ICT in organizations.

Fig. 2. Distribution of ICTSTRAT values by the existence of formal ITG (ISITDEPT).

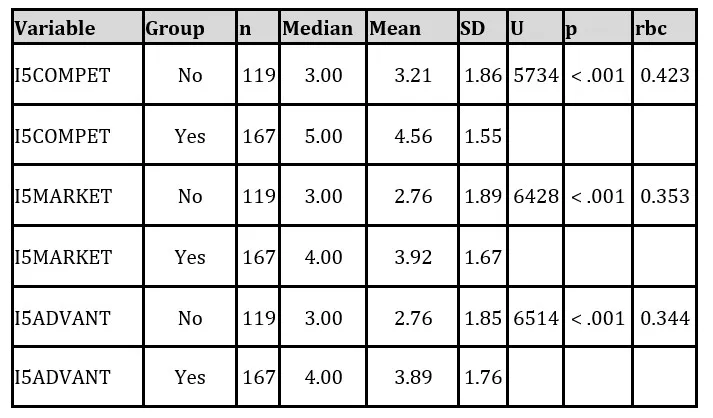

H2 hypothesized that organizations using economic metrics for IT evaluation would report higher perceived benefits of technological innovations in terms of competitiveness, responsiveness to market changes, and competitive advantage. The Mann-Whitney U test was used for verification, specifically for the variables I5COMPET, I5MARKET, and I5ADVANT; in multiple testing, p-values were adjusted using the Holm-Bonferroni procedure.

Table 3. Differences in perceived benefits by use of economic metrics

The results confirmed statistically significant differences between organizations that use economic metrics for IT evaluation and those that do not, in all three areas examined. For the I5COMPET variable, a significant difference was found (U = 5734, p < .001), with organizations using economic metrics achieving a higher median (Me = 5) than those not using them (Me = 3). The effect size was moderate to large (rbc = 0.423).

For the I5MARKET variable, the difference was also statistically significant (U = 6428, p < .001). Organizations using economic metrics reported higher values (Me = 4) than those not using them (Me = 3), with a moderate effect size (rbc = 0.353).

Similarly, a statistically significant difference was confirmed for the I5ADVANT variable (U = 6514, p < .001), with organizations using economic metrics for IT evaluation achieving a higher median (Me = 4) compared to organizations without economic IT evaluation (Me = 3). The effect size was moderate (rbc = 0.344).

Since all three differences remained statistically significant even after adjusting p-values using the Holm-Bonferroni procedure, H2 was supported. The results suggest that the use of economic IT evaluation metrics is associated with a higher perception of the benefits of technological innovations in strategically important areas of the organization’s operations.

These findings are consistent with Rubio-Andrés et al. (2025), who found a significant positive effect of digital transformation strategy on corporate innovation (β = 0.34, p 0.05), but IT management capabilities and strategic alignment are key mediators (β = 0.423, p < 0.001). This supports the interpretation that it is not IT resources themselves, but the way they are managed and evaluated, that determines whether organizations perceive the benefits of technological innovations.

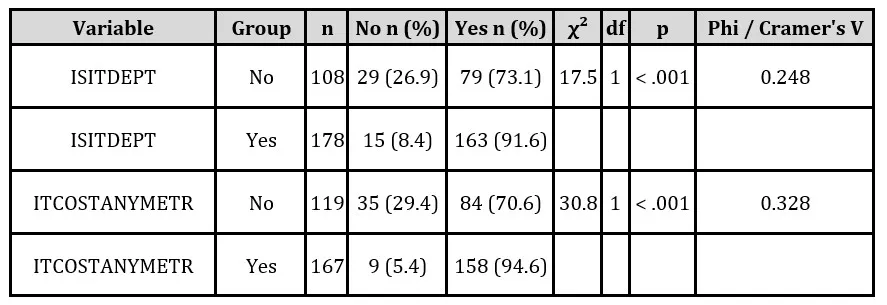

As a preliminary step in assessing H3, chi-square tests of independence were first used between the variables ISITDEPT and TECHCOSTYN, as well as between the variables ITCOSTANYMETR and TECHCOSTYN.

Table 4. Bivariate relationships between ITG, IT economic metrics, and reported reductions in operating costs

In both cases, a statistically significant relationship was demonstrated. A significant relationship was found between ISITDEPT and TECHCOSTYN, χ²(1, N = 286) = 17.5, p < .001, with an effect size of 0.248 according to Phi. Organizations with a formally established IT department reported a reduction in operating costs more frequently than organizations without an IT department. An even stronger relationship was found between ITCOSTANYMETR and TECHCOSTYN, χ²(1, N = 286) = 30.8, p < .001, Phi = 0.328, with organizations using IT economic metrics more frequently reporting a reduction in operating costs.

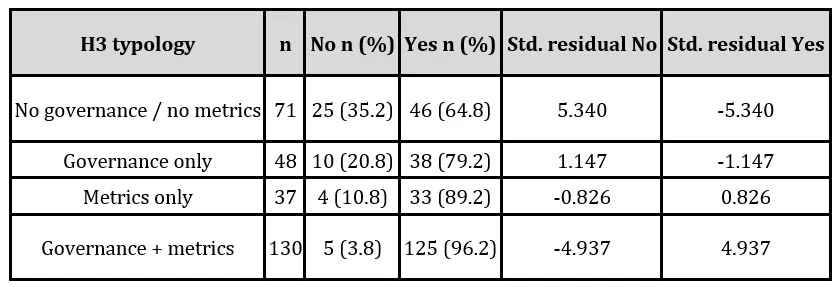

Subsequently, a 4-category typology of organizations was created combining the presence of ITG and economic metrics.

Table 5. Distribution of TECHCOSTYN responses by combination of ITG and economic IT metrics

The chi-square test revealed a statistically significant association between organization type and the TECHCOSTYN variable, χ²(3, N = 286) = 36.4, p < .001, with an effect size of 0.357 according to Cramer’s V. A post hoc analysis using standardized residuals showed that organizations without ITG and without economic metrics exhibited a significantly higher number of “No” responses and a lower number of “Yes” responses than would be expected given the independence of the variables. Conversely, organizations with ITG and with economic metrics showed a significantly lower number of “No” responses and a higher number of “Yes” responses than expected.

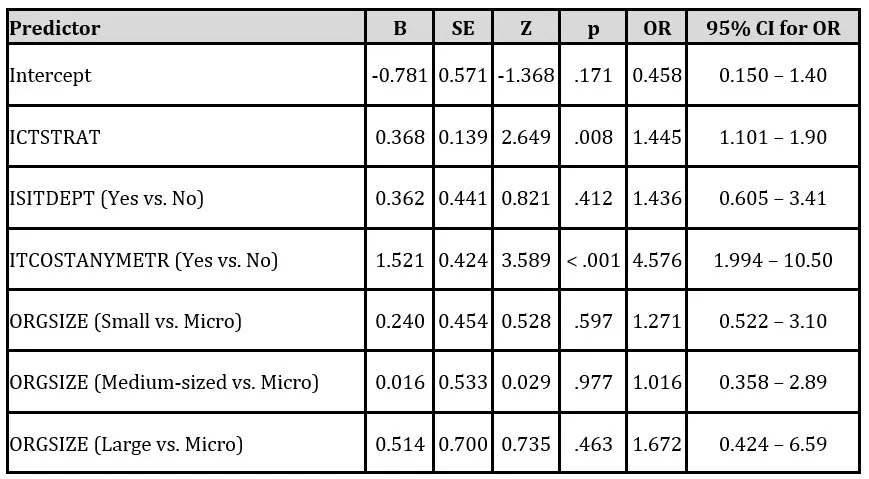

To test the hypothesis in a multivariate framework, binary logistic regression was used with the variable TECHCOSTYN as the dependent variable and the variables ISITDEPT, ITCOSTANYMETR, ICTSTRAT, and ORGSIZE as predictors (economic sector is introduced as a control in the hierarchical H4 model).

Table 6. Results of binary logistic regression for the probability of a reported reduction in operating costs (TECHCOSTYN = Yes)

The model was statistically significant, χ²(6, N = 286) = 44.8, p < .001. The level of ICT strategy (OR = 1.445, p = .008) and the use of IT economic metrics (OR = 4.576, p < .001) emerged as significant predictors. The existence of an IT department, after controlling for other variables, did not show a significant effect (OR = 1.436, p = .412). A supplementary model with the interaction term ISITDEPT × ITCOSTANYMETR did not confirm a statistically significant interaction effect (p = .859).

Model diagnostics for H3 showed the following characteristics: McFadden R² = 0.183 and Nagelkerke R² = 0.252, indicating that the model explains a substantial share of the variance in the binary dependent variable. Model fit was further supported by the omnibus likelihood-ratio test, χ²(6) = 44.8, p < .001. The Hosmer-Lemeshow test was not calculated for this model due to the low number of unique covariate patterns.

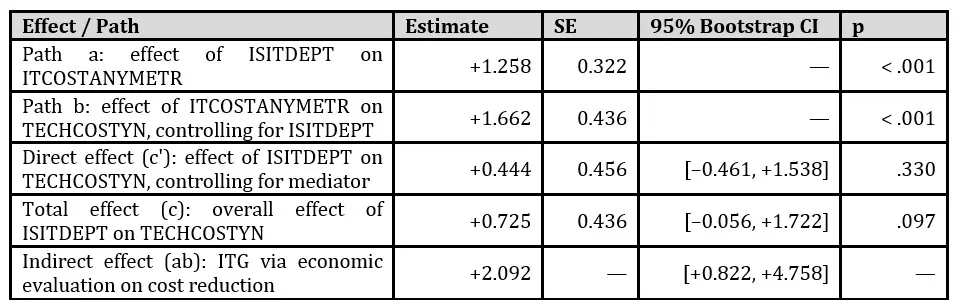

Using the bootstrap mediation procedure described in the Methodology section (Preacher and Hayes, 2008; Zhao, Lynch and Chen, 2010), we estimated the indirect, direct, and total effects of formal ITG (ISITDEPT) on reported operating cost reduction (TECHCOSTYN), with the use of economic IT evaluation metrics (ITCOSTANYMETR) as the mediator.

Path a (ISITDEPT → ITCOSTANYMETR) was statistically significant (β = 1.258, p < .001), indicating that organizations with formal ITG are substantially more likely to institutionalize the use of economic IT evaluation metrics. Path b (ITCOSTANYMETR → TECHCOSTYN, controlling for ISITDEPT) was also statistically significant (β = 1.662, p < .001), confirming that the systematic use of economic metrics predicts reported cost reductions even after accounting for the governance structure.

The indirect effect (ab) was estimated at +2.092 with 95% bootstrap CI [+0.822, +4.758], which excludes zero and thus confirms the existence of a significant mediation pathway. The direct effect (c’) of ISITDEPT on TECHCOSTYN, after controlling for ITCOSTANYMETR, was +0.444 with 95% CI [-0.461, +1.538], which includes zero and is not statistically significant. The total effect (c) was +0.725, 95% CI [-0.056, +1.722], also not significant at the conventional threshold. Detailed bootstrap outputs are reported in Table A3 (Appendix)

Following the mediation typology of Zhao, Lynch and Chen (2010), this pattern constitutes indirect-only mediation, a significant indirect effect combined with a non-significant direct effect. The near-zero total effect is a recognised property of such patterns, because the direct and indirect pathways can mask one another when the mediator is not modelled explicitly. The finding indicates that the association between formal ITG and reported cost reductions operates almost entirely through the institutionalized use of economic IT evaluation metrics, with no residual direct pathway. This formal statistical evidence strongly reinforces the interpretation offered in the H3 bivariate and multivariate results and is consistent with the resource complementarity argument developed in the Theoretical background.

H3 was supported. The bivariate and multivariate results suggested a potential indirect mechanism, which was formally confirmed by the bootstrap mediation analysis. The significant indirect effect combined with a non-significant direct effect indicates an indirect-only mediation pattern (Zhao, Lynch and Chen, 2010), implying that formal ITG contributes to reported cost reductions primarily through the institutionalized use of economic IT evaluation metrics.

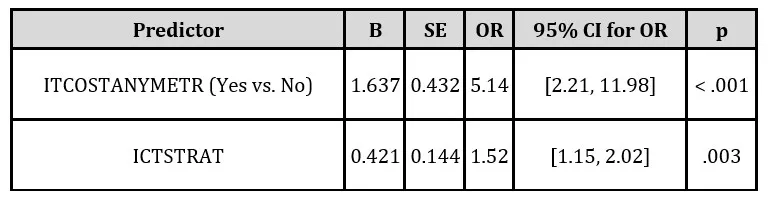

To test H4, a binary logistic regression was estimated with TECHCOSTYN as the dependent variable. In the first step, the control variables’ organization size and sector were included in the model. In the second step, the variables ISITDEPT and ITCOSTANYMETR were added, and, in the third step, the variable ICTSTRAT was also included. The final model was statistically significant, χ²(11) = 49.0, p < .001, with an explanatory power of Nagelkerke’s R² = .273.

Table 7. Binary logistic model for TECHCOSTYN – summary of significant results

After controlling for organization size and sector, the use of at least one economic metric for IT evaluation remained a significant positive predictor of reported operating cost reduction (OR = 5.14, 95% CI [2.21, 11.98], p < .001). The strategic role of ICT in the organization also emerged as a significant predictor (OR = 1.52, 95% CI [1.15, 2.02], p = .003). By contrast, formal ITG structure, operationalized as the presence of a separate IS/IT department or IT manager, had a positive but statistically non-significant effect (OR = 1.55, p = .333). These results indicate that only part of the tested associations remained robust after controlling for organization size and sector.

H4 was partially supported. After controlling for organization size and sector, the use of at least one economic IT evaluation metric (ITCOSTANYMETR, OR = 5.14, 95% CI [2.21, 11.98], p < .001) and the strategic role of ICT (ICTSTRAT, OR = 1.52, 95% CI [1.15, 2.02], p = .003) remained significant predictors of reported operating cost reduction. In contrast, the direct effect of formal ITG structure (ISITDEPT, OR = 1.55, p = .333) did not persist once the other variables were included in the model. These findings indicate that only part of the tested associations remained robust after controlling for organization size and sector.

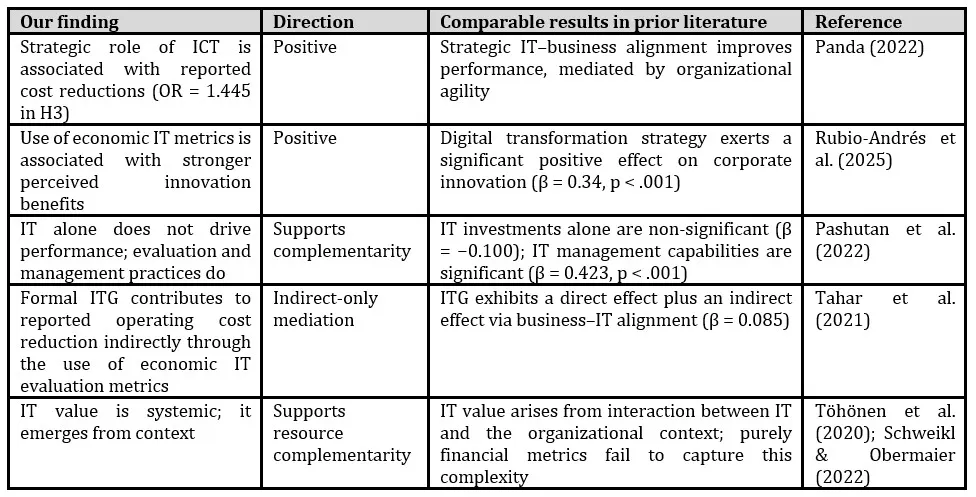

Table 8. Comparison of our findings with prior empirical literature

One of the most important findings of this study concerns the fact that the direct effect of ISITDEPT (existence of an IT department) became non-statistically significant in the multivariate model, while ITCOSTANYMETR (use of economic metrics) remained the dominant predictor. This pattern is consistent with resource complementarity (Schweikl & Obermaier, 2022): the mere existence of a governance structure is a necessary but not sufficient condition for creating value from IT. Formal ITG must be complemented by systematic economic evaluation of IT investments to translate into concrete cost savings. This finding is consistent with Tahar et al. (2021), who showed that the direct effect of ITG on performance (β = 0.259) is complemented by an indirect effect via business-IT alignment (β = 0.085), confirming the existence of a mediating mechanism. Similarly, Pashutan et al. (2022) found that IT investments alone do not have a direct significant effect on performance (β = –0.100, n.s.), whereas IT management capabilities do have a highly significant effect (β = 0.423, p < 0.001).

The results suggest that organizations should not focus exclusively on establishing an IT department or an IT manager position. The critical factor is whether the department possesses tools for systematic economic evaluation of IT investments and whether it uses these tools.

Practical Implications

Our results carry several implications for practitioners, policymakers, and professional associations operating in Slovak and broader Central European contexts.

For enterprise managers, the central message is that establishing a formal ITG structure, whether as a dedicated IS/IT unit or an IT manager role, is a necessary but insufficient condition for translating technology investments into measurable cost outcomes. Organizations that pair formal ITG with the institutionalized use of economic IT evaluation metrics (ROI, TCO, CAPEX, OPEX) are substantially more likely to report operational cost reductions (96.2% versus 64.8% in organizations with neither element). Priority investments should therefore target not only the creation of governance roles but also the development of financial evaluation discipline around IT decision-making.

For IT leaders, the 3.4-fold increase in the odds of perceiving ICT as strategic among organizations with formal ITG suggests that structural formalization reinforces the organizational narrative around IT as a strategic enabler. However, the direct effect of ITG on cost outcomes was not observed once economic evaluation was accounted for. This indicates that strategic positioning alone does not generate financial value; it must be operationalized through measurement and accountability mechanisms.

For policymakers and professional associations, particularly in the Central European context of ongoing digital transformation, these findings support targeted programmes that build financial controlling competencies for IT (e.g., certification aligned with COBIT or ISACA frameworks) and stimulate IT-governance maturity assessments in SMEs, which represent most of the Slovak enterprise base.

Regarding generalizability, the identified associations remained robust across organization size and sector, suggesting applicability to a broad cross-section of Slovak enterprises. At the same time, the sample is Slovakia-specific, with a notable share of industrial enterprises (21.7%) and a dominance of private ownership. Sector-specific patterns, for example the way heavy industry, retail, or professional services operationalize ROI versus TCO, likely warrant tailored frameworks. Potential risks include over-reliance on metrics that capture cost efficiency while under-valuing intangible strategic benefits, and the possibility that the observed associations partly reflect an unobserved general IT maturity capability rather than a direct causal chain. These possibilities should be investigated in longitudinal and multi-country follow-up studies.

Theoretical Contributions

This study offers three theoretical contributions. First, it empirically demonstrates the indirect-only mediation pattern (Zhao, Lynch and Chen, 2010) through which formal ITG shapes organizational outcomes. The bootstrap analysis (5,000 resamples) confirms that the direct effect of ITG on cost reduction is not statistically significant once the systematic use of economic IT evaluation metrics is controlled for, while the indirect path (ITG → metrics → cost reduction) is large and significant. This extends the traditional dynamic capabilities’ account (Harguem, 2021) by identifying economic evaluation as the concrete organizational routine through which governance capability is enacted.

Second, the study refines the resource complementarity explanation of the IT productivity paradox (Schweikl and Obermaier, 2022). Rather than treating management capabilities as a generic complement to IT, we show that the specific practice of institutionalized economic evaluation (ROI, TCO, CAPEX, OPEX) is the complementary mechanism that renders ITG effective in cost-related outcomes.

Third, the findings contribute Central European empirical evidence to a predominantly Anglo-American IT business value literature. The sample of 286 Slovak enterprises spanning multiple sectors and four size categories provides cross-sectional insight into how the governance–evaluation bundle operates in a transitional economy context, extending the generalization boundary of prior work (Bharadwaj, 2000; Wade and Hulland, 2004; Kohli and Grover, 2008).

Research Agenda

Several avenues extend this work. First, longitudinal designs would help establish temporal precedence in the governance–evaluation–outcomes’ chain and differentiate reciprocal relationships from one-directional mediation. Second, multi-country replications, particularly across Central and Eastern European countries, would test the external validity of the identified mediation pattern under varying institutional conditions. Third, future research should complement self-reported cost outcomes with objective financial indicators from registry data to address common method bias concerns. Fourth, the typology of Zhao, Lynch and Chen (2010) invites testing of competitive mediation scenarios in which other mechanisms (e.g., IT leadership capability, vendor management maturity) may partially offset the governance–evaluation pathway. Finally, given the accelerating transition toward Industry 5.0 (Nahavandi, 2019; Xu, Lu, Vogel-Heuser and Wang, 2021), the dynamic role of economic IT evaluation under human-centric, sustainability-oriented technology adoption deserves targeted investigation.

Limitations

The presented results must be interpreted within the context of limitations. The research was conducted on a sample of companies operating exclusively in Slovakia. The cross-sectional design does not allow for causal interpretations. The identified associations may be influenced by unmeasured variables. All data were collected via a self-report questionnaire, which carries a risk of common method bias. Harman’s one-factor model test showed that the first component explains 59.89% of the total variance, indicating a moderate risk of CMB; the results should therefore be interpreted with due caution. The questionnaire response rate was not reported, which limits the assessment of the sample’s representativeness. Future research could address these limitations through a longitudinal design, expanding the sample to an international level, and supplementing subjective measures with objective financial indicators.

The interpretation of the findings was not triangulated through structured consultation with industry experts. Although the statistical associations are robust and theoretically grounded, validation of the practical relevance of these patterns in the Slovak enterprise context (for example through focus groups with CIOs, IT managers, or IT-finance controllers) is left for future research. Such expert-driven triangulation would strengthen the ecological validity of our conclusions and help refine the practical implications outlined above.

A further methodological limitation concerns the role of ICTSTRAT in the multivariate models. Although it was included as a contextual organizational characteristic to test the robustness of the reported associations, ICTSTRAT may also be conceptually related to formal ITG as a downstream organizational attribute. Its inclusion should therefore be interpreted cautiously, as it may absorb part of the effect associated with formal ITG.

Conclusion

This study empirically verified the relationships between formal ITG, the use of economic metrics for IT evaluation, and organizational outcomes in a sample of 286 companies operating in Slovakia. The results yielded three main findings. First, formal ITG—operationalized as the presence of a separate IS/IT department or an IT manager—was significantly associated with the strategic perception of ICT in the organization (OR = 3.445, p < .001; H1). This finding is consistent with Elazhary et al. (2023) and Tahar et al. (2021). Second, organizations using economic metrics to evaluate IT reported significantly higher perceived benefits of technological innovations in terms of competitiveness, responsiveness to market changes, and competitive advantage (H2). Third, in the multivariate model, the decisive predictor of reported operating cost reduction was not the mere existence of an IT department (OR = 1.436, p = .412), but the use of economic IT evaluation metrics (OR = 4.576, p < .001). The formal bootstrap mediation analysis further showed that the relationship between formal ITG and reported operating cost reduction follows an indirect-only mediation pattern, with a significant indirect effect and a non-significant direct effect. This finding is consistent with resource complementarity (Schweikl & Obermaier, 2022) and indicates that formal ITG contributes to cost-related organizational outcomes primarily through the systematic economic evaluation of IT investments.

From a theoretical perspective, this study contributes to the literature on IT business value by empirically confirming that governance structures are a necessary but not sufficient condition for IT value creation, which is consistent with the dynamic capabilities’ perspective (Harguem, 2021) and resource complementarity (Schweikl & Obermaier, 2022). From a practical perspective, the results suggest that managers should view the establishment of an IT department and the implementation of IT economic valuation as complementary elements—investing in governance structures without simultaneously implementing a discipline for measuring IT value may lead to suboptimal returns. After controlling for organization size and sector, the associations of economic IT evaluation metrics and the strategic role of ICT with reported operating cost reduction persisted (H4), whereas the direct association of formal ITG did not. These results indicate that the cost-related effect of formal ITG is not robust as a direct predictor once the broader organizational context is taken into account, which is consistent with the indirect-only mediation identified above. Opportunities for further research include replicating the findings on an international sample, verifying the suggested mediating mechanism through structural modeling, and supplementing subjective measures with objective financial indicators of firms.

Data Availability Statement

The data that support the findings of this study are available from the corresponding author upon reasonable request, subject to restrictions related to the confidentiality of respondent-level organizational data.

Conflict of Interest

The authors declare that they have no known competing financial interests or personal relationships that could have appeared to influence the work reported in this paper.

Author Contributions

Conceptualization: M.Č., P.Š. and A.R.; Methodology: M.Č., P.Š. and A.R.; Formal analysis: M.Č. and P.Š.; Writing, original draft preparation: M.Č. and P.Š.; Writing, review and editing: M.Č., P.Š. and A.R.; Supervision: A.R. All authors have read and agreed to the published version of the manuscript.

Acknowledgments

The paper was prepared within the framework of VEGA No. 1/0520/24: Aspects of building an ambient enterprise ecosystem. 100% funding.

References

Adomako, S. and Nguyen, N.P. (2023) ‘Digitalization, inter-organizational collaboration, and technology transfer,’ The Journal of Technology Transfer, 49, 1176-1202.

Altman, D.G. and Bland, J.M. (2009) ‘Parametric and non-parametric methods for data analysis,’ BMJ, 338, a3167.

Barney, J. (1991) ‘Firm resources and sustained competitive advantage,’ Journal of Management, 17 (1), 99-120.

Baron, R.M. and Kenny, D.A. (1986) ‘The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations,’ Journal of Personality and Social Psychology, 51 (6), 1173-1182.

Bharadwaj, A.S. (2000) ‘A resource-based perspective on information technology capability and firm performance: An empirical investigation,’ MIS Quarterly, 24 (1), 169-196.

Eisenhardt, K.M. and Martin, J.A. (2000) ‘Dynamic capabilities: What are they?’ Strategic Management Journal, 21 (10-11), 1105-1121.

Elazhary, M., Popovič, A., Souza Bermejo, P.H. and Oliveira, T. (2023) ‘How information technology governance influences organizational agility: The role of market turbulence,’ Information Systems Management, 40 (2), 148-168.

European Commission. (2003) Commission Recommendation of 6 May 2003 concerning the definition of micro, small and medium-sized enterprises (2003/361/EC), Official Journal of the European Union, L 124, 36-41.

Hair, J.F., Black, W.C., Babin, B.J. and Anderson, R.E. (2019) Multivariate Data Analysis, 8th ed., Cengage Learning.

Harguem, S. (2021) ‘A conceptual framework on IT governance impact on organizational performance: A dynamic capability perspective,’ Academic Journal of Interdisciplinary Studies, 10 (1), 163-176.

Harris, J.K. (2021) ‘Primer on binary logistic regression,’ Family Medicine and Community Health, 9 (Suppl 1), e001290.

Hayes, A.F. (2017) Introduction to Mediation, Moderation, and Conditional Process Analysis: A Regression-Based Approach, 2nd ed., Guilford Press, New York.

Karataş, M.H. and Çakır, H. (2024) ‘A systematic literature review on IT governance mechanisms and frameworks,’ Journal of Learning and Teaching in Digital Age, 9 (1), 88-101.

Kohli, R. and Grover, V. (2008) ‘Business value of IT: An essay on expanding research directions to keep up with the times,’ Journal of the Association for Information Systems, 9 (1), 23-39.

Kumar V K, R., Ukko, J., Rantala, T. and Saunila, M. (2024) ‘The value of novel technologies in the context of performance measurement and management: A systematic review and future research directions,’ Data and Information Management, 8, 100054.

MacFarland, T.W. and Yates, J.M. (2016) ‘Mann-Whitney U test,’ in Introduction to Nonparametric Statistics for the Biological Sciences Using R, Springer, pp. 103-132.

Maia, A.L.M.D. and Frogeri, R.F. (2023) ‘Optimizing business value via IT governance mechanisms: An examination of SMEs in Southern Minas Gerais, Brazil,’ Journal of Operational and Strategic Analytics, 1 (3), 106-114.

Melville, N., Kraemer, K. and Gurbaxani, V. (2004) ‘Review: Information technology and organizational performance: An integrative model of IT business value,’ MIS Quarterly, 28 (2), 283-322.

Merín-Rodrigáñez, J., Dasí, À. and Alegre, J. (2024) ‘Digital transformation and firm performance in innovative SMEs: The mediating role of business model innovation,’ Technovation, 134, 103027.

Őri, D. and Szabó, Z. (2024) ‘A systematic literature review on business-IT misalignment research,’ Information Systems and e-Business Management, 22, 139-169.

Panda, S. (2022) ‘Strategic IT-business alignment capability and organizational performance: Roles of organizational agility and environmental factors,’ Journal of Asia Business Studies, 16 (1), 25-52

Pashutan, M., Abdolvand, N. and Rajaee Harandi, S. (2022) ‘The impact of IT resources and strategic alignment on organizational performance: The moderating role of environmental uncertainty,’ Digital Business, 2, 100026.

Patterson, M. (2020) ‘A structured approach to strategic alignment between business and information technology objectives,’ South African Journal of Business Management, 51 (1), a365.

Poldrack, R.A. (2018) Statistical Thinking for the 21st Century. [Online]. Russell Poldrack. [Retrieved 21 April 2026]. Available: https://statsthinking21.org/

Preacher, K.J. and Hayes, A.F. (2008) ‘Asymptotic and resampling strategies for assessing and comparing indirect effects in multiple mediator models,’ Behavior Research Methods, 40 (3), 879-891.

Rubio-Andrés, M., Linuesa-Langreo, J., Gutiérrez-Broncano, S. and Sastre-Castillo, M.Á. (2025) ‘Tackling digital transformation strategy: How it affects firm innovation and organizational effectiveness,’ The Journal of Technology Transfer, 50, 1893-1918.

Schweikl, S. and Obermaier, R. (2022) ‘Lost in translation: IT business value research and resource complementarity-an integrative framework, shortcomings and future research directions,’ Management Review Quarterly, 73, 1713-1749.

Tahar, A., Sofyani, H. and Kunimasari, D.P. (2021) ‘The role of IT governance and IT application orchestration capability on organizational performance during the COVID-19 pandemic: An intervening effect of business-IT alignment,’ JEMA: Jurnal Ilmiah Bidang Akuntansi dan Manajemen, 18 (1), 1-20.

Teece, D.J., Pisano, G. and Shuen, A. (1997) ‘Dynamic capabilities and strategic management,’ Strategic Management Journal, 18 (7), 509-533.

Töhönen, H., Kauppinen, M., Männistö, T. and Itälä, T. (2020) ‘A conceptual framework for valuing IT within a business system,’ International Journal of Accounting Information Systems, 36, 100442.

Wade, M. and Hulland, J. (2004) ‘Review: The resource-based view and information systems research: Review, extension, and suggestions for future research,’ MIS Quarterly, 28 (1), 107-142.

Xu, X., Lu, Y., Vogel-Heuser, B. and Wang, L. (2021) ‘Industry 4.0 and Industry 5.0-Inception, conception and perception,’ Journal of Manufacturing Systems, 61, 530-535.

Yang, X., Tu, H., Li, Y. and Wang, Q. (2025) ‘The impact of IT system implementation and upgrade on firm operational and financial performance,’ Journal of Digital Management, 1, 6.

Zhao, X., Lynch, J.G. and Chen, Q. (2010) ‘Reconsidering Baron and Kenny: Myth and truths about mediation analysis,’ Journal of Consumer Research, 37 (2), 197-206.

Note. X = ISITDEPT (formal ITG); M = ITCOSTANYMETR (use of at least one economic IT evaluation metric); Y = TECHCOSTYN (reported cost reduction). Covariates in both path models: ICTSTRAT, ORGSIZE, SECTORIND_TRANSFORMED. All path coefficients are reported on the log-odds scale.