Faculty of Economics and Business Administration, University of Craiova, A. I. Cuza St. No.13, Craiova, Romania;

Faculty of Business and Administration, Department of Economic and Administrative Sciences, University of Bucharest, Regina Elisabeta Boulevard, no. 4 – 12, sector 3, Bucharest, Romania;

Faculty of Economics, The Bucharest University of Economic Studies, Ion N. Angelescu Building, Piata Romana nr. 6, sector 1, Bucharest, Romania;

National Institute of Research and Development for Environmental Protection (I.N.C.D.P.M.), The Department of Natural and Technological Hazards, Splaiul Independentei, No. 294, sector 6, Bucharest, Romania

Volume 2019,

Article ID 509857,

Journal of Human Resources Management Research,

17 pages,

DOI: 10.5171/2019.509857

Received date: 26 October 2018; Accepted date: 26 December 2018; Published date: 15 April 2019

Academic Editor: Nicoleta Radneantu

Cite this Article as:

Cristina Raluca GH. POPESCU (2019)," "Intellectual Capital": Major Role, Key Importance and Decisive Influences on Organizations’ Performance ", Journal of Human Resources Management Research, Vol. 2019 (2019), Article ID 509857, DOI: 10.5171/2019.509857

The theme chosen for the scientific research “”Intellectual Capital”: Major Role, Key Importance and Decisive Influences on Organizations’ Performance” aims to study the definitions, role, importance, valences and components of intellectual capital, as well as intellectual capital’s decisive influence on the level of organizational performance. Moreover, this theme proves to be extremely representative for the accounting field, due to the fact that it emphasizes the fact that differences do exist between accounting-based performance and market-based performance when addressing intellectual capital performance and organizational performance. Furthermore, this scientific research has a decisive role in presenting different approaches related to intellectual capital at the level of organizations. In the same time, this work plays a key part in identifying and analyzing the role and influence of intellectual capital at the level of organizational performance, especially since intellectual capital is regarded as one of the most important sources of organizational performance, as well as organizational competitive advantage, leading to of competitiveness development. In addition, it should be mentioned that measuring intellectual capital in the accounting field is one of the most challenging research subjects these days. Under these circumstances, it should be noted that in recent years it has been concluded that the tangible assets of an organization are only a part of its wealth or, if an extrapolation is desired, tangible assets of organizations are only a part of the wealth of the countries. That is the reason why it is believed today that the accounting value of organizations was mistakenly perceived, therefore, it can be mentioned that the representation of accounting value at the level of organizations needs to be rethought. However, the issues related to organizational intellectual capital should address as well the accounting value of organizations, the economic and financial strength of organizations, the power of organizations in general, in the sense of the future potential of organizations, the organizational production processes, the potential of organizations to adapt to market demand, the new challenges and perspectives brought by the society-based approach on knowledge. In this context, the authors believe that intangible assets play an increasing role at the level of the organizations, and hence, the importance of our intellectual capital is nowadays growing tremendously.

Keywords: Keywords: intellectual capital, tangible assets, intangible assets, accounting value, investments, effectiveness, efficiency, performance, excellence, competitive advantage, competitiveness, new economy, economic and financial decline, organizational production processes, and knowledge-based society.

Introduction

This section provides the general background of the study and highlights the research motivation, additionally having the purpose of presenting, first of all, the relationship that exists between the tangible assets and the intangible assets of the organization, and, second of all, the role, importance, components and influences of the intellectual capital, as one of the key intangible assets on the performance of organizations.

Moreover, it should be mentioned here that there are major differences between tangible assets and intangible assets (in the present case between tangible assets and intellectual capital), which take into account, for example, aspects of the following type.

Firstly, a main aspect to be emphasized here is that the organization’s tangible assets have an intrinsic value independent of the person who observes them, submits them to the attention and analyzes them and, moreover, many of them devalue with the passage time.

Secondly, another aspect to be emphasized here is that the intangible assets of the organization – such as intellectual capital, for example – have a value depending on the person who observes them, submits them to their attention and analyzes them and, moreover, can gain value over time, especially as mankind crosses today the stage of the new knowledge-based economy, which has led to the diversification of production means, to new challenges in solving problems that are difficult to solve by classical methods in access, to the understanding and the use of information, but has also led to their transformation into knowledge at the level of organizations, to new methods of having competent staff, well-trained staff, etc. Regarding the general aspects concerning the scientific context and the motivation of the chosen topic, we consider that the aspects presented in the following lines should be considered:

Motivation 1. First of all, the scientific context and the motivation of the chosen theme take into consideration the personal and professional interest for the chosen subject, reflected in the following elements: the desire to deepen and complement the knowledge acquired to date (taking into account the current trends in scientific research, tendencies which are meant to emphasize more and more the importance of interdisciplinary issues for each subject); and the desire to analyze in concrete terms the elements related to the evaluation of intellectual capital and its influence on the performances of the companies, in the context in which this subject is extremely generous (fact demonstrated by the existing specialized literature) and at the same time allows the realization of an extensive research on the field in the near future in the following research papers (applicable both in the private institutions and in the public institutions).

Motivation 2. Second of all, the scientific context and the motivation of the chosen theme take into account both the importance of the topic and the actuality of the issue. The assessment of intellectual capital and its influence on company performance have key elements such as: competition, competitiveness, creativity, innovation, efficiency, effectiveness, performance, entrepreneurship (this period was considered by many analysts to be the “era of entrepreneurship”), and prosperous business (as the foundation of stability and economic growth). In addition, we consider that the issue of the concept of “intellectual capital” has not been sufficiently debated and analyzed, as the literature can be successfully enriched in this area, especially in the field of accounting. In this respect, over time, it can be noticed that issues related to “intellectual capital” have generated some controversy not onlly on its definition and classification, but also on the modalities of evaluation at the level of the organization or the representation at the practical level in accounting in an organization.

Literature Review and General Background

The literature review and general background show that there is a continuously growing interest in studying the aspects related to intellectual capital. Therefore, regarding the analysis of the knowledge stage on this theme, it can be noticed that the subject presents a great interest among specialists at national and international level.

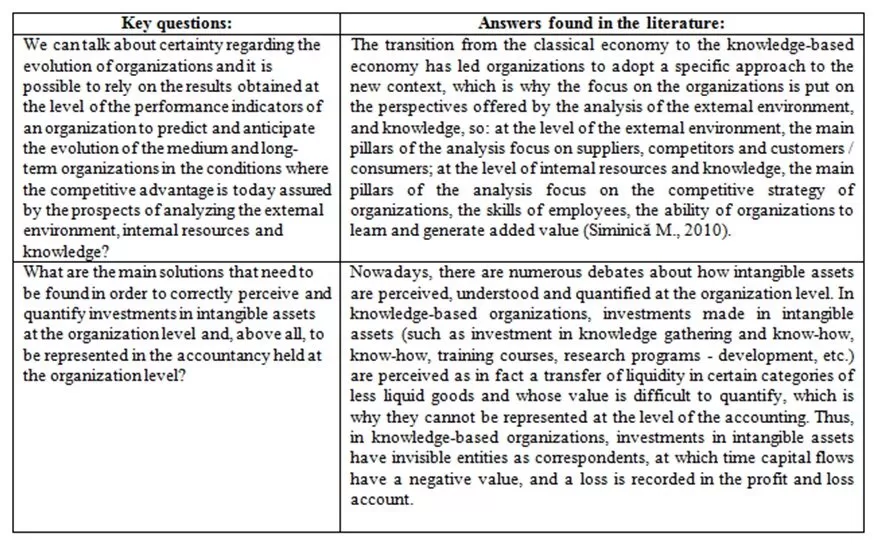

Table 1: “Intellectual Capital – key questions and answers found in the literature”

Source: the authors based on the sources mentioned

Moreover, the interest in this topic is the most diverse depending on the field the researchers are part of, as well as on the sphere of interest in which the studies they have made may fit. Furthermore, the specialized literature is extremely generous in dealing with topics such as human capital, intellectual capital, the capital represented by the clients of organizations, the performances of organizations, the role of human resources in the new knowledge-based economy and their impact on the performance of organizations, intellectual capital in the new knowledge-based economy and its impact on the performance of organizations (see, in this matter, Table no. 1: “Intellectual Capital – key questions and answers found in the literature”).

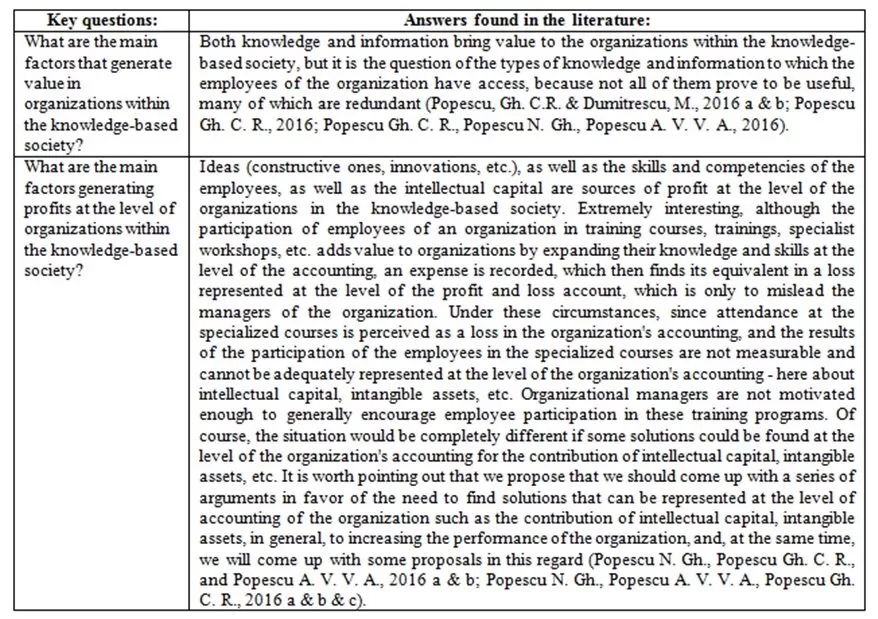

Previous studies have shown that at the core of organizations, whether they are smaller organizations or larger organizations or state or private organizations, both tangible assets and intangible assets, both types of assets, are designed to generate organization value. At the same time, prior research suggests that if elements such as tangible assets and intangible assets at the level of organizations, organizations and their level of performance, the knowledge of individuals working in organizations, and also the ability of organizations to learn, especially in a new economic, social and environmental environment generated by the new knowledge-based economy are desired, inevitably there will be a series of questions that need to be answered. Among these, we will mention here the most representative of our scientific approach, as follows in the lines below (see, in this matter, Table no. 2: “Intellectual Capital – key questions and answers found in the literature”).

Table 2: “Intellectual Capital – key questions and answers found in the literature”

Source: the authors based on the sources mentioned

A series of recent studies has indicated that both intellectual capital and knowledge management have the power to sustain organizational performance and, in the same time, to enable the organizations to become more competitive on the marketplace (Akpinar, A.T., and Akdemir, A., 2009).

Table 3: “Intellectual Capital and organizational performance – key connections”

Source: the authors based on the sources mentioned

This has been discussed by a great number of authors in the literature, some of them focusing on the relationship between intellectual capital and knowledge management and the organizational effectiveness (Marr, B., Gupta, O., Pike, S., Roos, G., 2003), others stressing the role of intellectual capital in creating and adding value to organizational performance (Bhatti, W. A. and Zaheer, A., 2008), and others being keen on emphasizing the connections that exist between intellectual capital and knowledge management and the organizational performance (Daud, S. and Yusoff, W.F.W., 2011) (see, in this matter, Table no. 3: “Intellectual Capital and organizational performance – key connections”).

“Intellectual Capital” and organizational performance – definitions, role, importance, key components and general influences

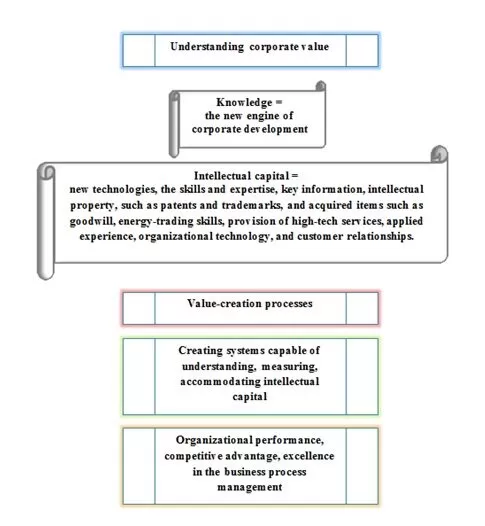

The section “Intellectual Capital” and organizational performance – definitions, role, importance, key components and general influences” presents the definitions, the role, the importance, the evaluation methods and the influences of the “intellectual capital” on the performance of the organizations, starting from the following premises (see, in this matter, Figure no. 1: “Performance of organizations: the role of intellectual capital and human capital”):

Step 1. The concept of “intellectual capital” is different from the concept of “human capital”, with definitions of the most varied and the most complex concepts related both to the concept of “intellectual capital” and to the concept of “human capital”. Even in these conditions where diversity is visible in the definition of these concepts, it is important to note that both intellectual capital and human capital are regarded as key components at the level of organizations without which their good work would be inconceivable in the current state.

Step 2. The concept of “intellectual capital” is one of the basic pillars of the knowledge-based economy. The role and importance of intellectual capital must be analyzed, discussed and debated in the context in which an increasingly fierce competition at the level of organizations is nowadays noted. In addition, the contribution of intellectual capital in the knowledge-based economy looks at key issues such as: improving organizational performance; increasing the visibility of some organizations in comparison with others, especially when it is possible to talk about the role of intellectual capital as a basic resource for increasing performance in organizations; increasing sustainability and, at the same time, increasing organizational sustainability (in the context of both increasing sustainability and increasing organizational sustainability), are generated by performance-related performance of organizations generated by intellectual capital influences.

Step 3. To our knowledge, “intellectual capital” can be evaluated by various methods, some of which are considered by specialists to be easy to represent and manage, and others are regarded as extremely complex and difficult to quantify elements in the organizations. At the same time, we are of the opinion that although intellectual capital can be evaluated through different methods at the level of organizations, not all of these methods can be applied to any type of organization, so diversity in these methods must be seen, understood and accepted as being directly linked to the diversity of the forms of organizations that exist worldwide and the concrete results they are targeting in the medium and long term.

Figure 1: “Performance of organizations: the role of intellectual capital and human capital”

Source: the authors

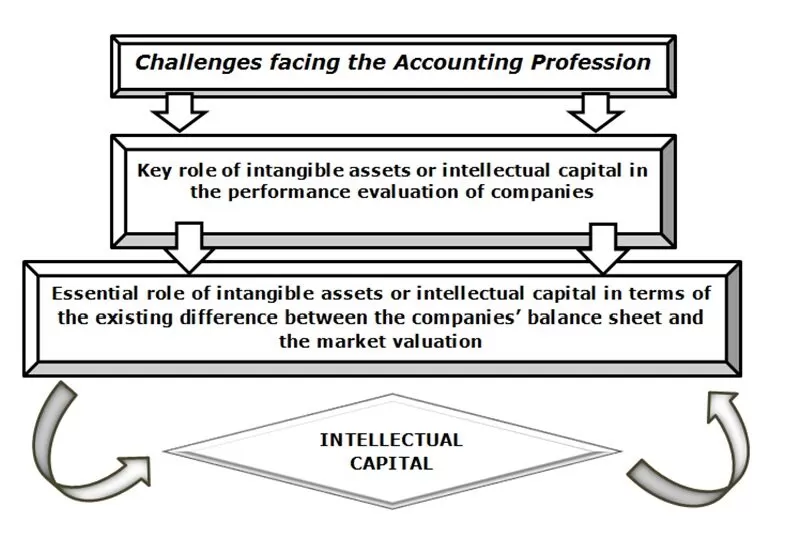

Step 4. Broadly speaking, “intellectual capital” decisively influences the performance of companies, having a key role at their level in the new context of the knowledge-based economy. Indeed, the new knowledge-based economy assigns a central role to both human capital and intellectual capital at the level of learning organizations. In this context, the skills of an organization’s employees, their competencies, and the knowledge that an organization’s employees use in processes that take place at the level of their structures, become essential in generating and ensuring organizational performance. At the same time, the skills, competencies and knowledge of employees used in an organization are intended to generate added value at the level of the organization, making it a competitive advantage compared to other competing organizations within the market (see, in this matter, Figure no. 2: “Challenges facing the Accounting Profession”).

Figure 2: “Challenges facing the Accounting Profession”

Source: the authors, adaptation after Figure 2: “Challenges facing the Accounting Profession” / p.7050, scientific paper entitled “”Intellectual Capital” – Role, Importance, Components and Influences on the Performance of Organizations – A Theoretical Approach”, author: Cristina Raluca Gh. Popescu, at the 32nd International Business Information Management Association (IBIMA) Conference, Seville, Spain, 15-16 November 2018 and published in the Proceedings Volume ISBN: 978-0-9998551-1-9 entitled “Vision 2020: Sustainable Economic Development and Application of Innovation Management from Regional expansion to Global Growth”, Editor Khalid S. Soliman, pp. 7045-7059

Organizational performance: “intellectual capital” versus “human capital” – key implications

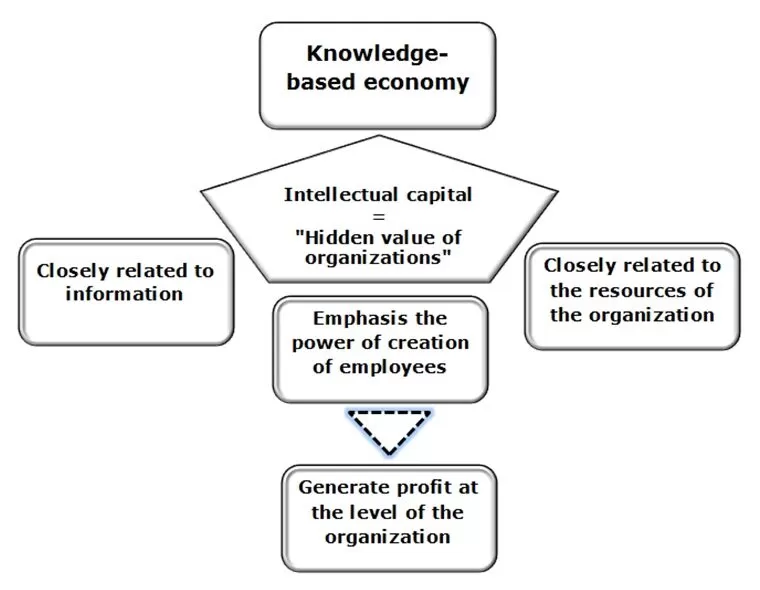

Within the section “Organizational performance: “intellectual capital” versus „human capital” – key implications” the key implications of the concepts of “intellectual capital” and “human capital” are presented with direct reference to the performance of organizations. Our intention is to put forward a series of arguments to support the assertion that the concept of “intellectual capital” is different from the concept of “human capital” (Bontis, N. (1996), Bontis, N. (1998), Bontis, N. (1999), Bontis, N., Dragonetti, N., Jacobsen, K. and Roos, G. (1999), Bontis, N., Keow, W. C. C. and Richardson, S. (2000), Bontis, N. (2001), Bontis, N. (2011), Bontis, N. and Fitzenz, J. (2002)). Thus, our approach will, in a first stage, be to present the definitions, role and importance of intellectual capital at the level of organizations and, in a second stage, to present the definitions, the role and the importance of human capital at the level of the organizations. The concept of “intellectual capital” is considered to be “the currency of the new millennium”; therefore, the optimal use of intellectual capital will be the key to success in the new knowledge-based economy. In addition, it is stated that in the new knowledge-based economy, intellectual capital is the “hidden value of organizations”, which was initially thought to be measurable and now has a number of ways to be either described, represented, appreciated, quantified and evaluated, depending on the domain we are referring to and the manner in which we perceive the assessments, and suggestions of the researchers in the field. There are a number of controversies about the moment when the concept of “intellectual capital” was used for the first time. In this respect, William J. Hudson (1993) is of the opinion that Gallbraith was the one who first used the concept of “intellectual capital” in his writings in 1958 (Hudson, W. (1993)). Equally, however, Thomas A. Stewart shares another view that the notion of “intellectual capital” dates back to 1958 (Stewart, T. (1998)). At the same time, according to a new perspective offered by Patrick H. Sullivan (2000), the term “intellectual capital” originates in 1980, when Hiroyuki Itami published the book “The Mobilization of Invisible Assets,” in Japanese (Itami H. and Roehl T.W. (1991)). Continuing the ideas presented in the above rows, Karl-Erik Sveiby (2001) notes in his studies that the issue of evaluating and measuring knowledge at an organization level was brought to the forefront by the Swedish group of Konrad companies (Sveiby, K.E. (2002), Sveiby, K. E. (1997), Sveiby, K. E., Lloyd, T. (1988)). The concept of “intellectual capital” has been recalled in the literature since the 1990s, when both its role and its importance in the world of business have become more and more obvious.

Table 4: “Intellectual Capital – perspectives and ways of viewing the concept”

Source: the authors

Moreover, it should be noted here that at that time, there were two ways of how specialists saw the concept of “intellectual capital”, both of which were related (see, in this matter, Table no. 3: “Intellectual Capital – perspectives and ways of viewing the concept” and Figure no. 3: “Intellectual Capital – the key role in the performance of organizations in the knowledge-based economy”). Of course, it can be noted that the knowledge-based organization is advocating for rethinking the organization’s set of values, changing the organization’s hierarchy of values, and defining a set of theories that position the organization’s intangible assets / resources at a higher level than tangible levels. In addition, nowadays, the intangible assets / resources of the organization within the knowledge-based organization are a determining factor in the development of society, in ensuring profitability at the level of companies, etc. As a matter of fact, the knowledge sector is the one that has recorded the highest growth, although to date there is no concrete way of quantifying human capital, intellectual capital and representation in the accounting balance sheet to the invisible share side.

Figure 3: “Intellectual Capital – the key role in the performance of organizations in the knowledge-based economy”

Source: the authors, Figure 3: “Intellectual Capital – the key role in the performance of organizations in the knowledge-based economy” / p.7052, scientific paper entitled “”Intellectual Capital” – Role, Importance, Components and Influences on the Performance of Organizations – A Theoretical Approach”, author: Cristina Raluca Gh. Popescu, at the 32nd International Business Information Management Association (IBIMA) Conference, Seville, Spain, 15-16 November 2018 and published in the Proceedings Volume ISBN: 978-0-9998551-1-9 entitled “Vision 2020: Sustainable Economic Development and Application of Innovation Management from Regional expansion to Global Growth”, Editor Khalid S. Soliman, pp. 7045-7059

It should be noted that the importance of intellectual capital should not be viewed and analyzed only at the level of an organization or a group of organizations. Essentially, in a knowledge-based society, intellectual capital becomes an integral part of national wealth, which implies that the value of the potential of human resources in a country at a given moment is given by the value of its intellectual capital. The structure of the national wealth system is extremely complex, which means that there are several basic components of it: human resources, natural resources, financial-currency resources, and material resources, etc. (Ahmed, R. B. (2003), Amir, E, and Lev, B. (1996)).

The concept of “intellectual capital” was first defined by Thomas A. Stewart; one of the members of the editorial board of the American magazine “Fortune”. In the opinion of specialists, the first appearance of the concept of “intellectual capital” in a press article can be found in the material entitled “Brain Power”, belonging to Thomas A. Stewart (1991). Thomas A. Stewart introduced and analyzed the concept of “intellectual capital” in several articles he published in the American magazine “Fortune”. In 1997, he published the book titled “Intellectual Capital: The New Wealth of Organizations” (in Romanian translation “Intellectual Capital: the New Rich of Organizations”), followed by the title “Wealth of Knowledge: Intellectual Capital and the Twenty-First Century Organization” (respectively, translated into Romanian” The Knowledge Wealth: Intellectual Capital and XXI Century Organization “).

According to a first definition of the concept of “intellectual capital,” it is viewed as a dynamic system formed both from intangible resources and activities that underpin the competitive advantage of organizations. In the opinion of specialists, this definition is considered to be incomplete at both the theoretical and practical level.

According to a second definition of the concept of “intellectual capital,” it is seen as a summing up of all the knowledge of an employee at an organization, in the context in which this knowledge is the basis for increasing its competitiveness and can generate, in the future, sources of increased competitiveness at the organization level. In the opinion of specialists, this definition is considered to be incomplete at both the theoretical and practical level.

Following the two definitions above, the rest of the definitions associated with the concept of “intellectual capital” are increasingly complex and establish, in turn, the links between “intellectual capital” and “human capital”, the knowledge-based economy, the organization which teaches – namely, the one whose profit cannot be generated in the absence of the ideas, skills and abilities of its employees or the intelligence of the individuals within it. Moreover, Charles Despres, Daniele Chauvel (1999) are of the opinion that the main production factor of today’s organizations is represented by knowledge, which is why the concept of “intellectual capital” should be viewed much deeper than, respectively, its intangible asset side of an organization, which involves associating it with a growth engine at the organization level based on a number of virtual, digital relationships and capable of delivering higher performance at the organization level (Despres C., Chauvel D. (1999)).

According to a third definition of the concept of “intellectual capital,” it is regarded as “knowledge that can be transformed into profit”, which means that there are a number of links between the intellectual assets of the organization and its intellectual capital after as follows (Sullivan, T.A. (1998), Bontis, N., Dragonetti, N., Jacobsen, K. and Roos, G. (1999)) (see, in this matter, Table no. 5: “Links between organizational intellectual assets and intellectual capital”):

Table 5: “Links between organizational intellectual assets and intellectual capital”

Source: the authors

According to a fourth definition of the concept of “intellectual capital,” it is perceived as the knowledge that can generate value at the organization level (Edvinsson, L. and Sullivan, M. (1997), Sullivan, T.A. (1998)). An example in this respect is that of organizations in the knowledge-based society that focus on innovation and value creation at the level of organizations, starting from information and then from knowledge. Thus, organizations in the knowledge-based society derive the benefit from innovation, and the performance they record is due to the way they select and capitalize on certain categories of knowledge. At the same time, it is worth noting that the market value of knowledge-based organizations exceeds their accounting value, precisely because this category of organizations operate with intangible assets that are hardly perceivable and valued at a time, but which are transformed into income.

Following the issues presented in the previous rows, there are a few questions that can form the basis for future analyzes and discussions, for example: Can intellectual capital – as a resource of the organization and the hidden value of organizations – anticipate how an organization will evolve?; Can intellectual capital – through its evaluation methods – determine whether an organization is going through a period of decline and at the same time help to avoid such a period?; and, Can intellectual capital – through its evaluation methods – positively influence the good progress of an organization and can lead to its success in the medium and long term?

Here too, it is necessary to define and analyze the concept of “human capital” in order to establish clearly and from the very beginning that there can be no sign of equality between the concept of “intellectual capital” and the concept of “human capital”.

The concept of “human capital” has several definitions, with a series of theories that address the role, importance, valences and influences of human capital at the level of organizations. Regarding the moment of the emergence of the concept of “human capital” at the level of the specialized economic literature, it should be noted that it occurred in 1961, when Theodore W. Schultz published the paper “Investment in Human Capital”. The way in which the term “human capital” is defined has been continuously improved, depending on the stages of humanity, the way in which each organization perceived the importance of human resources, the dimensions of its analysis, etc.

In these conditions, among the definitions of the notion of “human capital”, we mention, in the following ranks, the following elements which represent representative aspects of the classical theory of human capital:

Question 1. Firstly, according to a first definition, “human capital” refers to a person’s skills, abilities and knowledge to facilitate change in his / her actions;

Question 2. Secondly, in the sense of a second definition, “human capital” refers to the skills, abilities and knowledge of a person capable of leading to economic growth;

Question 3. Thirdly, as is apparent from a third definition, “human capital” refers to how a person’s capacities can be developed, improved, updated, renewed in a context facilitated by access to education, participation training courses, etc.

Going further in our analysis, the notion of “human capital” from the perspective of the neoclassical theory of human capital is associated with a new set of concepts, such as the economy of human capital or the new economy of human capital, human capital management, and human capital strategy, etc. In this respect, the notion of “human capital” from the perspective of the neoclassical theory of human capital takes into account aspects such as means and ways of managing the workforce, ways of motivating labor resources, sources of generation and maintenance in the medium term, and long-term management of an active and constructive management at the level of organizations, with the ultimate goal of increasing organizational performance and ensuring excellence in organizations (Anthony, J. H. and Ramesh, K. (1992)).

Therefore, a current definition of the term “human capital” is the following: “(1) the stock of professional knowledge, skills, abilities and health that can lead a person to increase his creative capacities and, implicitly, his expected income in the future; (2) the ability of people to produce materials and services efficiently” (Dicționar de economie, Ediția a II-a – A.S.E., 2009, Catedra de Economie şi Politici Economice, pag 234). Under these circumstances, according to this very first comprehensive definition of human capital, referral is made to the categories of professional knowledge – that is, to what employees need for the proper conduct of their workplace, and their skills and abilities that could lead to an improvement in their creative capacity which are all directly associated with revenue growth. At the same time, human capital has in mind the ability of individuals to produce materials and services efficiently, which automatically drives us with the concepts of efficiency, effectiveness , profitability, performance at the organization level.

Of course, the analysis of the notion of “human capital” at the level of an organization also requires distinctions in the types of human capital found in the specialized practice, as follows:

Step 1. A first type of human capital is the human capital specific to the individual. It focuses on the following specific aspects as follows: First, it takes into account the individual’s knowledge, skills and competencies that can be exploited both at the level of organizations and at the level of industrial branches or sub-branches; secondly, it refers to different categories of individual experience, such as managerial ones – respectively cases in which the individual held certain positions at the level of management of the organization, or the entrepreneurial one – respectively the cases where the individual had certain initiatives to implement a particular business, to be creative at the level of the organization to which it belongs, etc.; Third, it refers to the individual’s level of education, training, etc.; Fourthly, it refers to the general characteristics of the individual, such as his age, income, or family income.

Step 2. A second type of human capital is the human capital specific to an industrial branch. It focuses on the following specific aspects as follows: First, it takes into account the knowledge, skills and competencies of the individual’s need to work in a particular industrial branch; second, it takes into account the knowledge, skills and competencies of the individual acquired during the period in which they work in a particular industrial branch. In addition, it is worth mentioning here that researchers have emphasized at their level the idea that the experience of an individual working in a particular branch of industry is a plus at the level of the organization, which will be reflected in the economic growth, both at microeconomic and macroeconomic level, in an increase in the organization’s economic performance, etc. (Siegel, MacMillan (1993))

Step 3. A third type of human capital is the human capital of a large-scale organization. Under these circumstances, it should be stressed that the skills, competencies, knowledge of an individual that prove to be relevant to the position he or she occupies at the level of the respective organization forms the human capital specific to a large-scale organization (Arrow, K. J. (1999), Balkin, D. B. and Gomez-Mejia, L. R. (1984)).

Taking into consideration all the aspects presented above, a key question should be further taken into consideration: Will intellectual capital accounting revolutionize the economy?

The challenges brought by intellectual capital accounting are numerous, and are also strongly related to other important concepts such as: knowledge-based economy; management of intellectual capital; tools which are able to measure, plan and control the influence intellectual capital on an organization; effectively and efficiently functioning organizations; performance and excellence models focused organizations; and enhanced role of intellectual capital in the knowledge-based economy. Under these circumstances, the increasing role of intellectual capital accounting should be noted at an international level and also the importance of intellectual capital in the accounting field should be properly acknowledged. Moreover, the role of management accounting systems in the development of intellectual capital is crucial to the performance of organizations. Furthermore, by connecting intellectual capital with knowledge-based economy, accounting, management of intellectual capital, tools which are able to measure, plan and control the influence intellectual capital in an organization, effectively and efficiently functioning organizations, performance and excellence models focused organizations, enhanced role of intellectual capital in the knowledge-based economy, another element should also be considered: the organization’s capacity to innovate, and even in some cases to have a unique presence in the marketplace.

Conclusions and limitations

The scientific research paper entitled “”Intellectual Capital”: Major Role, Key Importance and Decisive Influences on Organizations’ Performance” takes into account the role, the importance and the influences that the intellectual capital has on the performance of organizations, acknowledging, in the same time, the fact that intellectual capital’s role in the accounting field is decisive. Moreover, this work emphasizes the way in which intellectual capital could be quantified and also makes a contribution to the accounting research by focusing on the definitions and tools to measure intellectual capital, as well as on the manner to properly manage human resources and intellectual capital. Furthermore, in the same time, the authors’ intention for a future research is to propose and suggest several ways in which several models of intellectual capital assessment can be analyzed at the level of the organizations and more means by which it can analyze, describe and quantify its influence on the performances of the companies (for the part applicative) covering both the sphere of private institutions and the sphere of public institutions from a national and international perspective. Certainly, it would be of great interest to carry out analyzes at the level of some R & D institutions in Romania and, at the same time, at the level of some private sector companies in Romania and abroad (even if they would choose both large companies and companies with a slightly more limited activity). This is the reason why we aim to make these analyzes that will make important contributions to our future scientific research project.

Acknowledgment

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors. Some of the contributions presented in this work were communicated and published in the scientific paper entitled “”Intellectual Capital” – Role, Importance, Components and Influences on the Performance of Organizations – A Theoretical Approach”, author: Cristina Raluca Gh. Popescu, at the 32nd International Business Information Management Association (IBIMA) Conference, Seville, Spain, 15-16 November 2018 and published in the Proceedings Volume ISBN: 978-0-9998551-1-9 entitled “Vision 2020: Sustainable Economic Development and Application of Innovation Management from Regional expansion to Global Growth”, Editor Khalid S. Soliman, pp. 7045- 7059.

Ahmed, R. B. (2003), Intellectual capital and firm performance of US multinational firms: a study of the resource-based and stakeholder views, Journal of Intellectual Capital, Vol. 4 Issue: 2, pp.215-226, Retrieved on 10th October 2018, from https://doi.org/10.1108/14691930310472839, https://www.emeraldinsight.com/doi/abs/10.1108/14691930310472839.

Amir, E., and Lev, B. (1996), Value-relevance of non-financial information: the wirelles communications industry, Journal of Accounting and Economics, Vol.22, No 1-3, pp.3-30, Retrieved on 10th October 2018, from https://www.sciencedirect.com/science/article/pii/S0165410196004302, https://doi.org/10.1016/S0165-4101(96)00430-2.

Anthony, J. H. and Ramesh, K. (1992), Association between accounting performance measures and stock: a test of the life-cycle hypothesis, Journal of Accounting and Economics ,Vol.15, pp.203-227, Retrieved on 10th October 2018, from https://doi.org/10.1016/0165-4101(92)90018-W, https://www.sciencedirect.com/science/article/pii/016541019290018W.

Arrow, K. J. (1999), Tehnical Information and Industrial Structure, in G.R. Carroll and David.J. Teeee (eds.), Firms. Markets and Hierarchies, Oxford: Oxford University Press. pp. 156-163.

Balkin, D. B. and Gomez-Mejia, L. R. (1984), Determinants of R & D compensation strategies in the high tech industry, Personnel Psychology, Vol.37, pp.635-650.

Bhatti W. and Zaheer A. (2008), The Role of Intellectual Capital in Creating and Adding Value to Organizational Performance: A Conceptual Analysis, The Electronic Journal of Knowledge Management, Volume 12, Issue 3 (pp187-194), Retrieved on 10th October 2018, from www.ejkm.com.

Bontis, N. (1998), Intellectual capital: an exploratory study that develops measures and models, Management Decision, Vol. 36 Issue: 2, pp.63-76, https://doi.org/10.1108/00251749810204142, https://www.emeraldinsight.com/doi/abs/ 10.1108/00251749810204142, accessed on 04.06.2018.

Bontis, N. (1999), Managing Organizational Knowledge by Diagnosing Intellectual Capital: Framing and Advancing the State of the Field, International Journal of Technology Management 18, 5/6/7/8: 433–462, Retrieved on 10th October 2018, from https://www.sciencedirect.com/science/article/pii/B9780750674751500063.

Bontis, N., Dragonetti, N., Jacobsen, K. and Roos, G. (1999), The knowledge toolbox:a review of the tools available to measure and manage intangible resources, European Management Journal, Volume 17, Issue 4, August 1999, Pages 391-402, Retrieved on 10th October 2018, from https://www.sciencedirect.com/science /article/pii/S0263237399000195, la https://doi.org/10.1016/S0263-2373(99)00019-5.

Bontis, N., Keow, W. C. C. and Richardson, S. (2000), Intellectual capital and business performance in Malaysian industries, Journal of Intellectual Capital, Vol. 1 Issue: 1, pp.85-100, Retrieved on 10th October 2018, from https://doi.org/10.1108/14691930010324188, https://www.emeraldinsight.com/doi/abs/10.1108/14691930010324188.

Bontis, N. (2001), Assessing knowledge assets: a review of the models used to measure intellectual capital, International Journal of Management Reviews, Vol.3, No.1, pp.41-60, Retrieved on 10th October 2018, from https://doi.org/10.1111/1468-2370.00053.

Bontis, N. (2011), World Congress of Intellectual Capital Readings, Routledge 2 Park Square, Milton Park, Abingdon, Oxon OX14, 4RN 711, Third Avenue, New York, NY 10017, USA.

Bontis, N., Crossan, M. and Hulland, J. (2002), Managing an organizational learning system by aligning stocks and flows, Journal of Management Studies,Vol.39, No.4, pp.437-469, Retrieved on 10th October 2018, from https://doi.org/10.1111/1467-6486.t01-1-00299.

Bontis, N. and Fitzenz, J. (2002), Intellectual capital ROI: a causal map of human capital antecedents and consequents, Journal of Intellectual Capital, Vol. 3 Issue: 3, pp.223-247, Retrieved on 10th October 2018, from https://doi.org/10.1108/14691930210435589.

Daud, S. and Yusoff, W.F.W. (2011), How intellectual capital mediates the relationship between knowledge management processes and organizational performance?, African Journal of Business Management, 5(7), 2607-2617, Retrieved on 10th October 2018, from https://academicjournals.org/journal/ajbm/article-abstract/893483828941.

Despres C., Chauvel D. (1999), Knowledge management(s), Journal of Knowledge Management 3(2):110-123, DOI: 10.1108/13673279910275567, Retrieved on 10th October 2018, from https://www.researchgate.net/publication/ 242025358_Knowledge_managements.

Edvinsson, L. and Sullivan, M. (1997), Intellectual Capital: The Proven Way to Establish Your Company’s Real Value by Measuring its Hidden Brainpower, Biddles Ltd, Guildford, King’s Lynn and London.

Hudson, W. (1993), Intellectual capital: How to build it, enhance it, use it, NY: John Wiley & Sons, Publisher: Wiley, Language: English, ISBN-10: 0471558133, ISBN-13: 978-0471558132.

Itami H. and Roehl T.W. (1991), Mobilizing Invisible Assets, Cambridge: Harvard University Press (reprint edition), ISBN 9780674577718.

Marr, B., Gupta, O., Pike, S., Roos, G. (2003), Intellectual capital and knowledge management effectiveness, Management Decision, Vol. 41, Issue: 8, pp.771-781, Retrieved on 10th October 2018, from https://doi.org/10.1108/00251740310496288

Popescu Gh. C. R. & Dumitrescu, M. (2016, a), The Importance of Change Typology – a Key Element in the Enterprise’s Organizational Dynamics, Revista “Manager Journal”, nr. 23/2016, pp. 116 – 123, http://manager.faa.ro/en/volumes/Manager-23–2016~105.html, ISSN-L 1453-0503, ISSN (e) 2286-170X și ISSN (p) 1453-0503.

Popescu Gh. C. R. & Dumitrescu, M. (2016, b), A New Configuration: Management’s Paradigms – Acting in the Context of Social Economy, Revista “Manager Journal”, nr. 23/2016, pp. 124 – 137, http://manager.faa.ro/en/volumes/Manager-23–2016~105.html, ISSN-L 1453-0503, ISSN (e) 2286-170X și ISSN (p) 1453-0503.

Popescu Gh. C. R., Contributions Regarding The Study And Evaluation Of Interdependencies Between Key Factors In Increasing The Competitiveness (în limba engleză), Editura Mustang, Bucureşti, 2016, 290 pagini, ISBN 978-606-652-102-4; link: http://www.editura-mustang.ro/carti_universitare.php.

Popescu Gh. C. R., Popescu N. Gh., Popescu A. V. V. A., The business environment of the companies – nowadays perspectives, advantages and challenges, The 8th edition of the International Conference on Economics and Administration (ICEA 2016), 4 – 5 November 2016, link: http://icea-conference.eu/icea/index.php/2015/07/07/the-2016-international-conference-on-economics-and-administration/, Editura Universităţii din Bucureşti (“University of Bucharest” Publishing House), pp. 95 – 106, ISSN: 2284 – 9580, ISSN-L: 2284 – 9580.

Popescu N. Gh., Popescu Gh. C. R., and Popescu A. V. V. A., (2016 a), The Macro Environment and the Companies’ Economic, Social and Research – Development – Innovation Potential – Nowadays Key Elements, Perspectives and Challenges, Revista “Manager Journal”, nr. 24/2016, http://manager.faa.ro/en/volumes/Manager-23–2016~105.html, ISSN-L 1453-0503, ISSN (e) 2286-170X și ISSN (p) 1453-0503.

Popescu N. Gh., Popescu Gh. C. R., and Popescu A. V. V. A., (2016 b), The microenvironment, a key component of the companies’ external business environment – a nowadays diverse, complex and dynamic perspective, The 8th edition of the International Conference on Economics and Administration (ICEA 2016), 4 – 5 November 2016, link: http://icea-conference.eu/icea/index.php/2015/07/07/the-2016-international-conference-on-economics-and-administration/, Editura Universităţii din Bucureşti (“University of Bucharest” Publishing House), pp. 107 – 116, ISSN: 2284 – 9580, ISSN-L: 2284 – 9580.

Popescu N. Gh., Popescu A. V. V. A., Popescu Gh. C. R., (2016 a), Locul, rolul, importanţa şi influenţele comerţului asupra mediului de afaceri naţional şi internaţional din perspectiva economiei, a managementului şi a marketingului (în limba română), Editura C.H. Beck, Bucureşti, 2016, 94 pagini, ISBN 978-606-18-0611-9.

Popescu N. Gh., Popescu A. V. V. A., Popescu Gh. C. R., (2016 b), The relations, differences and controversies between “economic growth”, “economic development” and “sustainable development” – the case of Romania (în limba engleză), Editura C.H. Beck, Bucureşti, 2016, 62 pagini, ISBN 978-606-18-0610-2.

Popescu N. Gh., Popescu A. V. V. A., Popescu Gh. C. R., (2016 c), Managementul comercial și managementul forțelor de vânzare – o abordare din perspectiva provocărilor mediului de afaceri contemporan, Editura Mustang, Bucureşti, 2016, 398 pagini, ISBN 978-606-652-103-1; link: http://www.editura-mustang.ro/carti_universitare.php.

Sveiby, K. E. (1997), The New Organizational Wealth: Managing and Measuring Knowledge-Based Assets, Berrett-Koehler Publishers; 1st edition, San Francisco, USA, Language: English, ISBN-10: 1576750140, ISBN-13: 978-1576750148.